Smart Contract Insurance: How Blockchain Is Redefining Trust

The insurance world still battles delays, disputes, and distrust. Smart contract insurance is solving these problems with automation and transparency powered by blockchain. This MOR Software’s guide explains how it’s reshaping insurance operations and rebuilding customer trust.

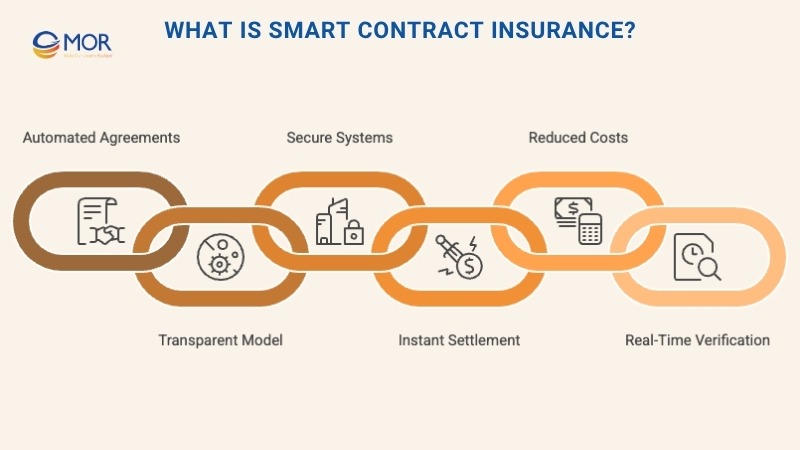

What Is Smart Contract Insurance?

Smart contract insurance is a blockchain-powered agreement that automatically releases payments once specific, pre-defined conditions are fulfilled. Over the past decade, this technology has matured into a transparent, data-driven model similar to modern parametric insurance systems. These smart contracts in insurance operate on immutable blockchain networks, guaranteeing fairness and accuracy in every transaction.

Because these agreements run within decentralized systems, they are inherently secure, tamper-resistant, and verifiable by all involved parties. The payout process happens directly on the blockchain platforms, and funds are transferred only when all pre-set conditions are satisfied. This automation minimizes disputes and delays, creating faster and more reliable claim settlements.

Unlike traditional policies that rely on intermediaries, insurance smart contracts eliminate the need for third-party involvement, cutting administrative overhead and reducing policy premiums. Every transaction, condition, and payout is recorded transparently, offering both insurers and policyholders complete visibility into the process.

In essence, smart contracts insurance defines the terms between two parties just like any conventional policy would, but with an added layer of automation and accountability. The system continuously tracks claims, verifies data in real time, and ensures that both sides meet their obligations without manual intervention. This combination of transparency and automation is what makes blockchain smart contracts insurance a turning point for the industry.

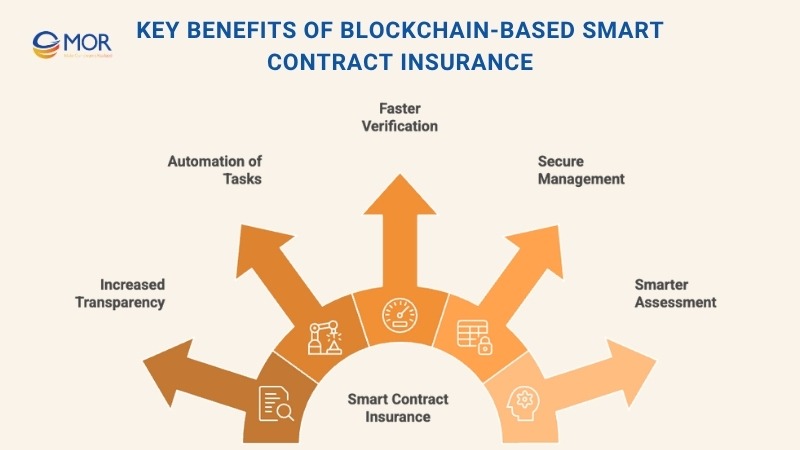

Key Benefits Of Blockchain-Based Smart Contract Insurance

The rise of smart contract insurance is pushing insurers worldwide to rethink how they manage claims, policies, and customer trust. As blockchain technology gains traction, it’s helping insurance firms unlock higher transparency, speed, and reliability across operations. The real payoff comes from automation, data integrity, and a drastic cut in manual errors that have long slowed down the industry.

Transparency That Prevents Fraud

One of the biggest strengths of smart contracts for insurance lies in the foundational pillar of blockchain security - blockchain’s decentralized and public nature. Every transaction recorded on the blockchain is visible to authorized participants, making it nearly impossible to alter or forge data. Since no single party owns or controls the system, any change becomes instantly traceable. This shared visibility builds trust and minimizes fraud, as discrepancies are detected right away by everyone in the network.

Automation Of Routine Tasks

Blockchain smart contracts insurance removes the need for human input in claim validation and payout processes. Once predefined rules are met, the contract executes automatically, ensuring accuracy and consistency. This eliminates manipulation risks and administrative inefficiencies. Insurers benefit from a smoother, faster workflow where approvals, verifications, and settlements happen transparently within the blockchain network, leading to greater convenience for both companies and customers.

Faster Claim Verification

Smart contract insurance replaces traditional manual claim reviews with automated validation on the blockchain. Once all predefined conditions are satisfied, the payout is triggered instantly without requiring paper documents or human intervention. This automation saves time, increases accuracy, and reduces administrative expenses, allowing insurers to deliver faster resolutions and improved customer experiences.

Secure Policy Record Management

With insurance smart contracts, critical policy data can be stored across multiple distributed ledgers, making it nearly impossible to alter or lose. Each record is encrypted and backed by blockchain’s immutable design, which prevents unauthorized access and data corruption. This ensures that every document, from policies to claims, remains fully traceable, verifiable, and permanently accessible when needed.

Smarter Risk Assessment

The integration of blockchain in insurance enables companies to use advanced, data-driven risk models within smart agreements. A blockchain-based identity system verifies user information in real time, eliminating redundant manual checks. Through smart contract trigger mechanisms of decentralized insurance, insurers can instantly access verified data, analyze risk levels, and tailor policy decisions accordingly. This digital process streamlines assessment efforts, strengthens accuracy, and supports more reliable underwriting.

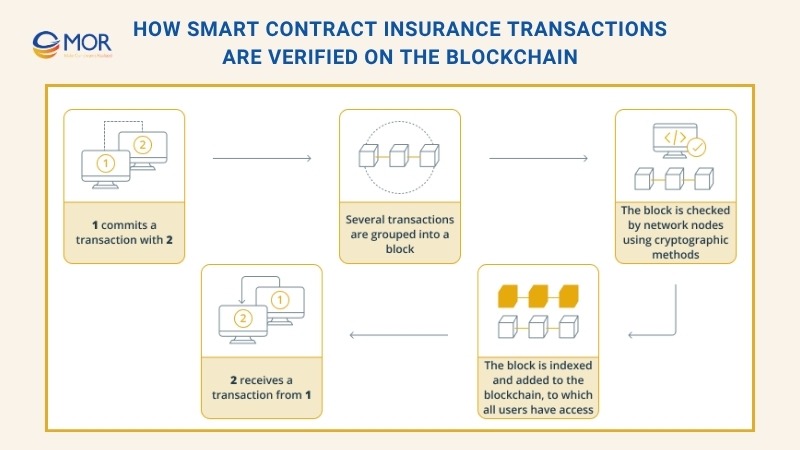

How Does Smart Contract Insurance Work?

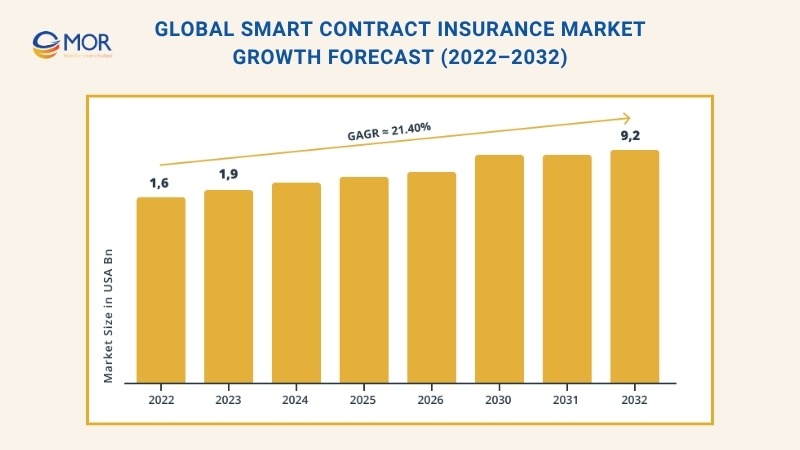

Recent research from Market Research Future projects the global smart contract insurance market to hit around 9.2 billion USD by 2032, expanding at a 21.4% CAGR between 2023 and 2032. This surge reflects the growing trust in blockchain services industries like banking, healthcare, real estate, and especially insurance.

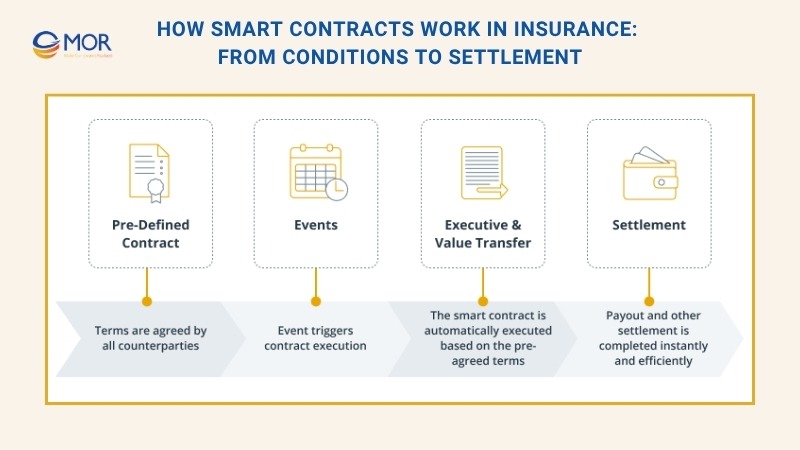

In this sector, smart contracts in insurance function as self-executing digital agreements that follow cryptographically verified rules. Each contract includes pre-defined conditions, events, and settlement procedures. Once these triggers are met, payouts are made automatically, without third-party involvement or manual validation.

The need for insurance smart contracts is growing as trust issues remain a major concern in the industry. A Harris Poll in the U.S. revealed low satisfaction levels among policyholders: 42% for Gen Z, 43% for Millennials, and 46% for Gen X. Many customers assume insurers avoid paying claims, while companies face fraud and exaggerated claims from policyholders. This lack of confidence affects both sides.

That’s where smart contracts insurance changes the game. By embedding business rules into code, blockchain automates claim validation and payouts through transparent logic that can’t be manipulated. These cryptography insurance protocols ensure every transaction is verified, reducing the need for middlemen and restoring fairness across the process. For insurers, this means fewer administrative delays; for customers, it builds renewed trust through consistent, data-backed actions.

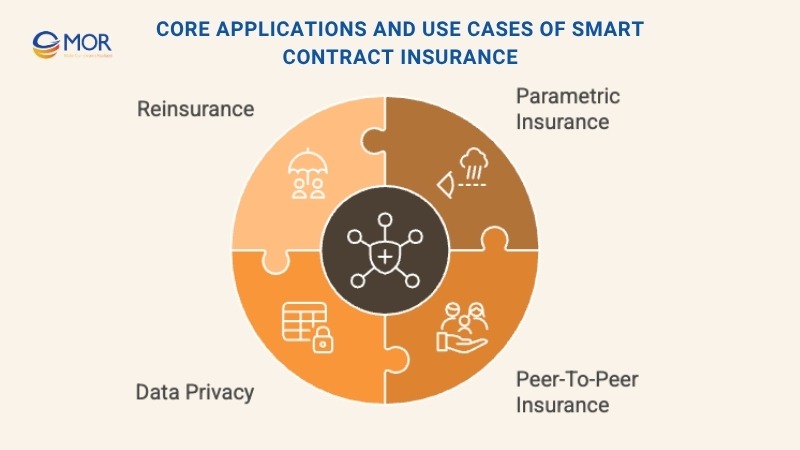

Core Applications And Use Cases Of Smart Contract Insurance

Smart contract insurance relies on blockchain as its technological foundation, allowing automatic claim settlements once specific rules are met. These coded agreements remove the need for manual oversight or third-party verification. Every step, from detecting an event to issuing payments, is executed transparently through blockchain protocols. This creates a faster, fairer, and more reliable experience for both insurers and policyholders.

Parametric Insurance

In smart contracts insurance, parametric or index-based models pay out when a defined event happens, not after loss evaluation. For instance, if a storm or earthquake reaches a specified magnitude, the contract triggers payment automatically. External data providers, or oracles, confirm these real-world events on the blockchain. Once confirmed, the smart contract trigger mechanisms of decentralized insurance activate, releasing funds instantly. This model speeds up compensation, reduces disputes, and improves customer satisfaction through data-backed objectivity.

Peer-to-Peer Insurance

In blockchain smart contracts insurance, the peer-to-peer model allows groups, like families, communities, or small businesses, to pool resources and insure each other. The agreement terms are written directly into the smart contract, defining contribution amounts, claim criteria, and payout rules. When a claim occurs, the code validates it automatically and distributes payments based on the pre-set terms. This digital collaboration minimizes administrative costs and strengthens transparency among members, bringing a sense of shared accountability to modern smart contracts for insurance.

Data Privacy

In smart contract insurance, protecting sensitive information is a top priority. Blockchain acts as a secure, tamper-proof ledger that maintains the accuracy and integrity of all records. By storing verified data collected through oracles, insurers can confidently manage information used to assess eligibility for parametric payouts. Each transaction is encrypted, time-stamped, and permanently recorded, guaranteeing reliability and trust across the network. This same transparency fosters confidence among participants in peer-to-peer models, ensuring shared accountability without exposing personal details.

Reinsurance

In large-scale insurance operations, reinsurance acts as a safety net for insurers managing substantial risks. With blockchain in insurance, reinsurance contracts become clearer and faster to execute. Smart contracts automatically verify terms, track shared liabilities, and trigger payments once specified events occur. This reduces paperwork, delays, and the risk of human error. The immutable design of digital asset insurance transactions ensures that data exchanged between partners remains secure, fraud-free, and instantly verifiable, creating a more efficient and trustworthy reinsurance ecosystem.

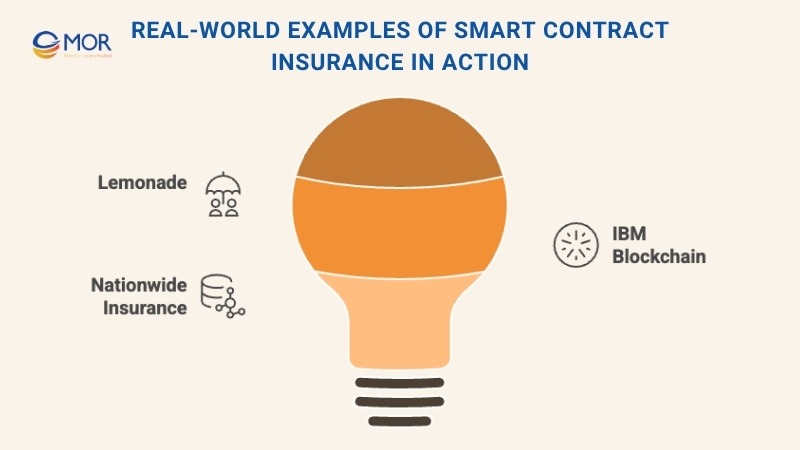

Real-World Examples Of Smart Contract Insurance In Action

The rise of smart contract insurance with the increase of blockchain software development company, smart contract insurance is no longer a distant concept. Leading insurers and insurtech firms are already integrating blockchain technology into real-world applications, transforming how claims are managed and payouts are made. These innovations demonstrate how automation and transparency can reshape trust in the insurance ecosystem.

Lemonade

In 2022, the insurtech company Lemonade introduced the Lemonade Crypto Climate Coalition, a blockchain-powered initiative designed to deliver affordable climate insurance to smallholder farmers in developing regions, beginning with Africa. This program uses the Avalanche blockchain, known for its energy-efficient proof-of-stake mechanism, to help farmers file and track claims directly through mobile devices.

Daniel Schreiber, Director of the Lemonade Foundation, explained the project’s vision: “By using a DAO instead of a traditional insurance company, smart contracts instead of insurance policies, and oracles instead of claims professionals, we can harness the decentralized power of Web3 and real-time weather data to deliver fair, instant coverage where it’s needed most.”

This initiative stands as a strong smart contract insurance example, showing how blockchain can support transparent, data-driven protection for vulnerable communities and make protecting digital assets and real-world livelihoods equally accessible.

IBM Blockchain

IBM may not be a traditional insurer, but its IBM Blockchain initiative has become a key enabler for blockchain smart contracts insurance solutions. In 2017, IBM partnered with AIG to launch the first multinational smart contract policy for Standard Chartered Bank PLC. This groundbreaking project created a unified, real-time platform for managing policy terms and documentation across multiple jurisdictions.

The blockchain setup simplified insurance administration between the United Kingdom, the United States, Singapore, and Kenya, each with distinct legal frameworks and compliance standards. By using blockchain, IBM and AIG demonstrated how insurance smart contracts can synchronize data, improve transparency, and handle complex, cross-border insurance operations efficiently.

Nationwide Insurance

Nationwide, one of the largest U.S. insurance providers, has also embraced smart contracts insurance through its collaboration with the RiskBlock Alliance. The company became the first major insurer to apply blockchain for policy automation and claims processing. Using bitcoin insurance principles and verified data sources, Nationwide’s blockchain-based contracts allow claim verification through official law enforcement records. Once validated, payouts are executed automatically, cutting down on time, paperwork, and potential disputes while enhancing policyholder confidence in the process.

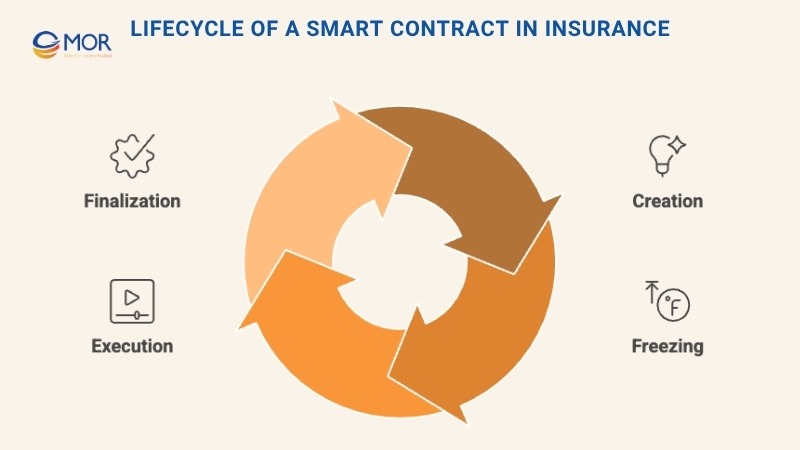

Lifecycle Of A Smart Contract In Insurance

Regardless of the sector, every smart contract insurance system follows four essential phases that define how agreements are created, validated, and completed on the blockchain. These stages ensure accuracy, transparency, and fairness throughout the contract’s entire digital journey.

Creation

In this stage, the involved parties agree on all policy details, rules, and expected outcomes. Once finalized, the agreement is translated into code, forming a smart contracts in insurance program that automatically enforces the predefined conditions. Developers encode every term clearly to prevent ambiguity and ensure smooth execution later on.

Freezing

After deployment, the contract becomes visible on the blockchain ledger and enters an immutable state. Both parties must meet all outlined terms, such as transferring funds, submitting data, or validating identities, to activate the process. During this period, assets or payments linked to the smart contracts for insurance remain locked in secure wallets until all requirements are satisfied.

Execution

Once the predefined conditions are fulfilled, the blockchain initiates the next step. New transactions are automatically recorded in the distributed ledger and verified through consensus mechanisms. This guarantees that no data is altered or duplicated, ensuring reliable automation across every claim or payout event in smart contract insurance.

Finalization

When all obligations are met, assets are released, and the contract reaches completion. The blockchain records every transaction permanently, confirming full transparency and compliance. This smart contract insurance example of automation not only finalizes payouts efficiently but also reinforces accountability and trust between insurers and policyholders.

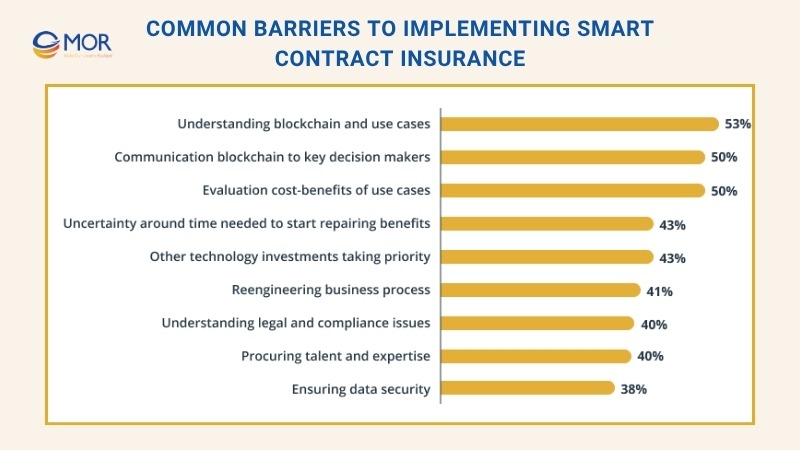

Common Barriers To Implementing Smart Contract Insurance

Even though blockchain has been around for years, its large-scale use in industries like insurance is still maturing. Many insurers see the potential of smart contract insurance, but adopting it as a fully dependable business solution comes with challenges. Understanding these limitations helps companies prepare better for real-world deployment.

Limited Flexibility In Contract Design

The biggest obstacle to using smart contracts in insurance lies in how rigid coding structures can be. Each possible event must be predefined in the program, and while that works well for simple logic, complex policy terms can be harder to represent in code. Many insurers begin with basic “if X, then Y” automation, which limits how nuanced real-world claims or exceptions can be handled within a digital system.

Technical Complexity

Developing blockchain smart contracts insurance solutions demands advanced programming expertise, particularly in blockchain frameworks like Ethereum. Crafting secure and scalable contracts requires precise code logic and a deep understanding of distributed networks. This makes it difficult for traditional insurance firms without in-house blockchain engineers to implement the technology smoothly. Moreover, technical complexity also create high solidity audit price.

Coding Errors And Reliability Risks

Although automation reduces human intervention, errors can still occur during development. Insurance smart contracts run sequentially, so even one missing or miswritten line of code can halt execution or cause unintended results. Testing, auditing, and version control become essential to avoid costly disruptions. In short, while blockchain minimizes fraud, it can’t eliminate human error in coding entirely.

Legal And Regulatory Uncertainty

The insurance sector is heavily regulated, yet most regions lack clear legal guidelines for smart contracts insurance. Governments are still exploring how these digital agreements fit into existing frameworks. Without standardized rules, insurers face uncertainty around compliance, dispute resolution, and enforceability. Establishing consistent regulations will be critical for large-scale adoption of blockchain in insurance systems.

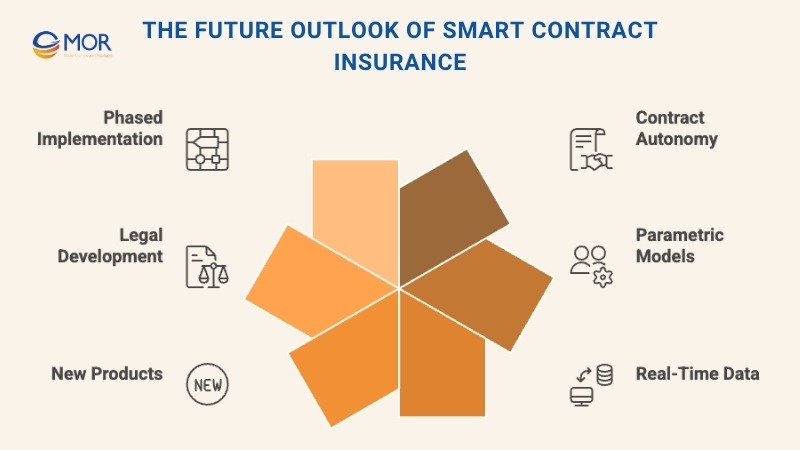

The Future Outlook Of Smart Contract Insurance

Smart contract insurance is moving the industry toward automation, accuracy, and instant trust. Manual paperwork is giving way to data-driven code that executes contracts automatically. With blockchain and AI working together, insurers will soon handle claims, pricing, and risk evaluation in real time. The next decade will blend innovation, compliance, and smarter digital infrastructure that reshapes how insurers interact with customers.

- Full Contract Autonomy: Future insurance smart contracts will manage entire policy lifecycles, from creation to payout, without human oversight. AI integration will allow these contracts to analyze data, detect patterns, and make adaptive decisions on coverage and claims.

- Parametric And Collaborative Models: As parametric insurance expands, payouts will rely on measurable events like rainfall or flight delays. Blockchain technology will power community-driven coverage models governed by transparent tokenized incentives, strengthening decentralized trust among participants.

- Integration With Real-Time Data: IoT sensors and trusted oracles will feed live information into blockchain smart contracts insurance, making fraud detection and premium adjustments instant. Continuous data exchange between on-chain and off-chain systems will become the backbone of modern smart contracts for insurance.

- New Insurance Products: Expect growth in micro-insurance, pay-per-use policies, and coverage for digital assets. This new flexibility will serve both emerging and developed markets, helping insurers personalize protection while protecting digital assets with precision.

- Regulatory And Legal Development: As automation expands, lawmakers will refine policies to define accountability, transparency, and privacy standards. Verified, open-source code and independent audits will play a major role in maintaining confidence in smart contracts insurance systems.

- Phased Implementation: Many insurers will begin with parameter-based products like travel or weather insurance before scaling into hybrid systems that blend blockchain automation with traditional contracts.

Ultimately, smart contract insurance represents more than just a tech trend. It’s a shift toward fairness, real-time service, and operational trust. Insurers adopting this model early will lead the market in speed, efficiency, and customer credibility.

>>> Discover many more blockchain use cases like smart contract

MOR Software – Trusted Partner for Smart Contract Insurance Solutions

At MOR Software, we empower insurers to adopt smart contract insurance securely and effectively. Our blockchain experts have hands-on experience across Ethereum, Polygon, and Hyperledger, delivering automated systems that handle everything from data validation to claim processing with precision and transparency.

Blockchain Consulting and Integration

We offer strategic consulting to help insurers build a clear roadmap for blockchain adoption. Our engineers connect your existing systems, CRM, customer data, and payment platforms, with blockchain-driven insurance smart contracts, ensuring seamless integration and operational harmony.

Custom Smart Contract Development

We develop tailored contracts for parametric, peer-to-peer, and reinsurance models. Each smart contract insurance example is built with transparency, traceability, and high security to comply with international standards and industry regulations.

Automation and AI-driven Optimization

By combining blockchain with AI and IoT, we create self-updating systems that allow smart contracts for insurance to validate data, detect risks, and trigger claims automatically. This approach minimizes manual work and improves decision-making in risk management.

Continuous Support and Scalability

Our support doesn’t stop at deployment. MOR Software provides ongoing maintenance, scaling solutions, and compliance updates. Our team keeps your blockchain smart contracts insurance systems optimized for performance, reliability, and future regulatory alignment.

Ready to transform your insurance operations? Contact us today to discuss how MOR Software can help you design and deploy your next-generation smart contract insurance solution.

Conclusion

Smart contract insurance is redefining how insurers build trust, automate claims, and deliver transparency to customers. As blockchain technology continues to mature, insurance businesses that act early will gain a strong competitive edge in speed, accuracy, and credibility. At MOR Software, we specialize in building secure, scalable blockchain systems that turn innovation into real business outcomes. Contact us today to start developing your smart contract in insurance solution.

MOR SOFTWARE

Frequently Asked Questions (FAQs)

What are smart contracts in insurance?

Smart contracts in insurance are self-executing digital agreements built on blockchain. They automatically enforce rules, validate conditions, and execute actions based on predefined terms between multiple parties. These contracts streamline workflows, ensure compliance, and reduce manual errors across insurance operations.

How can blockchain be used in insurance?

Blockchain enhances insurance processes by enabling secure, instant, and automated payments between customers, insurers, and third-party providers. It cuts settlement times from days to seconds while ensuring that payment data remains accurate and fully protected.

How does blockchain improve insurance claims processing?

Blockchain speeds up claims processing by allowing real-time verification and shared access to transaction data. Because every record is stored transparently on a distributed ledger, disputes and delays decrease, and both insurers and policyholders can rely on consistent, trusted information.

What is the metaverse in insurance?

The metaverse in insurance applies virtual and augmented reality to create new digital experiences. Insurers can assess virtual risks, design protection for digital assets, and connect with customers through immersive 3D environments.

How can the blockchain help make insurance business more efficient?

Blockchain and smart contracts automate tasks such as underwriting and claims management, reducing paperwork and manual handling. This leads to faster processing, lower costs, and greater efficiency across all insurance functions.

How is blockchain used in insurance?

Blockchain supports the insurance industry by using smart contracts to track policies, automate documentation, and secure data. It strengthens transparency, enhances efficiency, and ensures that customer and transaction information cannot be altered.

What is the blockchain for auto insurance?

In auto insurance, blockchain improves data sharing among drivers, insurers, and service centers. It accelerates documentation, strengthens data protection, reduces costs, and builds trust by ensuring all records remain consistent and tamper-proof.

What is the meaning of blockchain in banking and insurance?

Blockchain in banking and insurance acts as a decentralized, tamper-resistant ledger that securely records and tracks transactions. It provides a single source of truth, boosts transparency, and safeguards data across the entire financial and insurance ecosystem.

Share

Rate this article

0

over 5.0 based on 0 reviews

Your rating on this news:

Name

*Email

*Write your comment

*Send your comment

1