AI in Wealth Management: Complete Guide 2026

Are you looking to enhance operational efficiency and deliver more personalized financial services? In today’s increasingly competitive landscape, integrating AI in wealth management is no longer optional; it’s a strategic imperative for your business. This MOR Software's article provides a comprehensive overview of AI in finance to ensure regulatory compliance and decision-making transparency.

What Is AI In Wealth Management?

AI in wealth management refers to the use of artificial intelligence technologies to analyze financial data, generate insights, and support decision-making processes. Unlike traditional systems that follow pre-programmed rules, AI can learn from big data analytics platform, detect behavioral patterns, and adapt its responses in real time.

A key distinction lies between AI and traditional automation. While both aim to improve efficiency, their capabilities differ significantly:

Criteria | Traditional Automation | Artificial Intelligence in Wealth Management |

Operating model | Rule-based, follows fixed instructions | Learns from data, adapts, and improves over time |

Data processing | Limited, mostly structured, and linear | Handles big data, unstructured, and real-time inputs |

Flexibility | Low – can't respond to unexpected scenarios | High – reacts to new data and shifting behaviors |

Application in wealth management | Basic tasks like reporting or data entry | Strategic functions like forecasting and personalization |

Human involvement | High – relies on manual oversight | Lower – depending on automation level and governance |

Key Advantages Of Using AI In Wealth Management

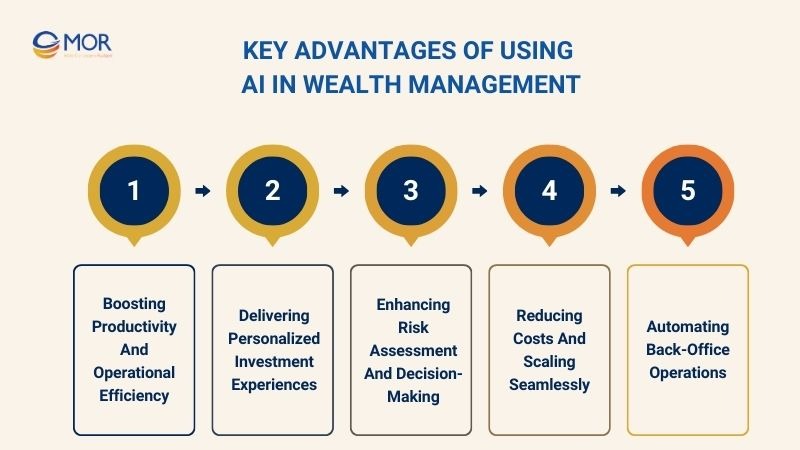

The adoption of AI in wealth management has become a core driver of transformation for modern financial firms. Below are the most prominent benefits of the use of AI in wealth management that every organization should seriously consider implementing.

Boosting Productivity And Operational Efficiency

AI wealth management enables financial institutions to automate a wide range of repetitive tasks such as data collection, transaction processing, identity verification, and periodic report generation. 80% of financial advisors plan to leverage AI to automate time-consuming tasks, highlighting the growing reliance on intelligent systems to drive efficiency.

What sets AI automation apart is its ability to perform these tasks continuously, 24/7, without manual intervention. This not only shortens processing time and improves accuracy, but also frees up human teams to focus on more strategic, value-driven initiatives.

Delivering Personalized Investment Experiences

Traditional investment advisory models typically group clients into broad categories and then offer similar recommendations to everyone in the same group. However, AI is completely transforming this approach by enabling personalized investment strategies tailored to each individual, based on behavioral data, financial goals, and risk tolerance.

For example, a young customer with a moderate income whose goal is to buy a house within the next three years. AI would likely suggest allocating most of their assets into fixed-term savings products, short-term bonds, or low-volatility investment funds. This ensures capital preservation and steady returns, well-aligned with their short-term financial objective.

Enhancing Risk Assessment And Decision-Making

AI in wealth management enables systems to aggregate and analyze vast amounts of data from diverse sources, including market trends, financial news, and even social media activity, to detect unusual signals or emerging patterns. This capability is especially valuable during periods of market volatility, where manual analysis can be slow or emotionally biased.

AI-powered tools provide advanced risk modeling and simulation, allowing wealth managers to test multiple “what-if” scenarios. As a result, investors can proactively prepare for potential downturns, rather than simply reacting after the fact.

Reducing Costs And Scaling Seamlessly

One clear advantage of AI in wealth management is its ability to reduce overall operational costs. For example, instead of relying on a large team of market analysts, AI can process data and generate consolidated reports within seconds.

JPMorgan Chase revealed that its AI tools have delivered approximately $1.5 billion in cost-saving benefits across areas like fraud detection, trading, and credit analysis

Automating Back-Office Operations

Departments like compliance, internal audit, and operations often consume substantial resources due to their need for precision and strict oversight. The use of AI in wealth management for these functions enables firms to automate report generation, regulatory compliance monitoring, and transaction verification.

The benefits go beyond time savings; AI also reduces legal risk and enhances transparency. Additionally, AI systems can maintain clear audit trails, which are valuable for internal reviews and third-party inspections. This reinforces accountability while streamlining traditionally labor-intensive back-office processes.

>>> Are you struggling to manage your growing wealth efficiently? Explore the best wealth management apps offer secure, AI-powered solutions.

Real-World AI Use Cases In Wealth Management

AI in wealth management is no longer a future technology. It’s already in use and transforming how financial firms operate. The following AI use cases in wealth management will give you a complete view of this ongoing shift.

Improving Client Retention And Engagement

AI in wealth management helps predict churn risk by analyzing customer behavior across transactions, app activity, and communication responses. This enables firms to launch timely, personalized engagement campaigns—an essential factor for improving client loyalty and long-term retention.

AI in wealth management examples: At XYZ Bank, a monthly AI-powered review is conducted to evaluate customer engagement.

The AI system analyzes behavior data such as login frequency, transaction volume, email interaction, and product usage levels.

- If a client hasn’t made any transactions in the past 60 days -> the AI system flags them as a “high churn risk and automatically routes the case to the customer success team

- If a customer has clicked on an investment banner but didn’t complete registration -> AI automatically sends a personalized follow-up email with recommended portfolios based on their risk profile and financial goals.

Crafting Personalized Investment Strategies

Unlike traditional methods that group clients into broad categories, AI in wealth management allows for highly individualized investment planning. The system analyzes each client’s financial goals, risk tolerance, and spending behavior to build tailored strategies. When input data changes, AI automatically adjusts portfolios in real-time, ensuring alignment with each client’s evolving financial profile.

Example: A 35-year-old client inputs personal financial data into a wealth management app:

- Monthly income of 40 million VND

- Goal to buy a house in five years, and a low risk appetite.

AI workflow:

- The AI system processes this and recommends an initial allocation: 70% into long-term bonds, 20% into money market funds, and 10% into dividend-focused mutual funds.

- Eight months later, AI detects lower monthly spending, higher account balances, and frequent searches for tech stocks. It identifies a shift in risk appetite.

- The system automatically revises the strategy, increasing tech stock exposure from 0% to 15%, while showing a risk disclaimer. A notification appears: “Your portfolio has been adjusted based on your latest behavior. View now?”

- If the client approves, the AI rebalances the portfolio instantly. If not, it waits and re-prompts after one week.

Optimizing Portfolios And Asset Allocation

AI in wealth management can analyze large-scale market data to recommend optimal asset allocation strategies. It also enables automatic portfolio rebalancing in response to market volatility. Machine learning models identify risks and opportunities faster than traditional methods.

Example: An investor holds a portfolio with 60% equities and 40% bonds.

- The AI system continuously updates real-time market data, including price movements, interest rates, and global economic news.

- When the stock market begins to correct sharply, the AI detects high-risk signals and automatically alerts the investor: “Recommendation: Reduce equity exposure to 45% to preserve capital.”

- Upon confirmation, the system rebalances the portfolio, reducing equity exposure, increasing bond allocation, and allocating 10% into a money market fund.

- The AI then activates active monitoring to rebalance again if further market changes occur.

Detecting Fraud And Managing Risk Proactively

AI in wealth management plays a critical role in monitoring trading behavior and detecting anomalies in real time. The system can flag potential risks such as fraud, market manipulation, or unauthorized access before they cause damage. In addition, AI simulates various market scenarios to support proactive risk management and mitigation.

Example: A client suddenly initiates a large international money transfer, despite having a consistent history of small, local transactions.

- AI detects this abnormal activity by comparing transaction amount, frequency, and location against the client’s historical behavior.

- The system cross-references the transaction with fraud detection models trained on millions of previous cases and flags it as high risk.

- Instantly, an alert is sent to the risk control team, and the transaction is temporarily suspended.

- At the same time, an automated verification message is sent to the client to confirm the legitimacy of the transaction.

- If the client does not respond or denies the activity, the AI system automatically locks account access and logs the incident for further investigation.

AI-Powered Financial Planning And Advice

AI in wealth management also enables long-term financial planning. Instead of relying on manual consultations, users can now interact directly with AI-powered chatbots via financial platforms or apps.

These systems analyze data such as income, spending habits, and personal goals to generate tailored recommendations for saving, investing, and budgeting.

A notable example is MoMo, a popular e-wallet in Vietnam. It uses AI to study users’ financial behavior and suggest optimal income allocation. If a user overspends on dining, the system will flag the issue and recommend reducing that category.

It might also advise setting aside 10–20% of income for savings or insurance, depending on financial capacity. When income patterns change, the AI automatically updates the financial plan to stay aligned with the user’s situation.

Navigating Compliance With AI In Wealth Management

In wealth management, implementing AI requires more than just efficiency; it must also comply with legal frameworks and ethical standards. Below are key regulatory considerations firms must keep in mind:

Building Ethical AI Governance Frameworks

An AI governance framework refers to a structured set of policies, procedures, and oversight mechanisms to regulate how AI systems are developed. The goal is to ensure that AI in financial services remains transparent, fair, and free from ethical or legal risks.

A critical component of this framework is establishing an internal AI ethics board. This board typically includes representatives from departments such as AI/IT, legal and compliance, internal audit, and risk management. Its key responsibilities include:

- Developing ethical AI principles that guide model design and deployment, such as non-discrimination, explainability, and data protection.

- Conducting regular evaluations of AI models to identify bias, unintended behavior, or compliance risks.

- Reviewing and approving AI applications before implementation in investment, advisory, or financial analysis processes.

- Reporting and recommending adjustments when models violate internal policies or industry standards.

Firms can align their practices with globally recognized AI governance standards such as the OECD AI Principles, MAS FEAT (Singapore), or NIST’s AI Risk Management Framework (U.S.) to ensure responsible AI deployment in wealth management.

Ensuring Data Privacy And Regulatory Alignment

AI in wealth management is only sustainable when strict data protection regulations are followed. Depending on the region, firms must comply with frameworks such as GDPR in Europe, CCPA in the U.S., or local laws like Vietnam’s Cybersecurity Law.

This is especially critical as AI systems often process sensitive financial data, including personal investment records and transaction histories. As of early 2025, EU supervisory authorities have issued a total of €5.88 billion (~$6.17 billion USD) in GDPR fines related to data privacy violations.

Maintaining Human Oversight In AI Decision-Making

While AI in wealth management can quickly analyze data and generate recommendations, human oversight remains essential. Regulatory bodies such as the SEC (United States) and ESMA (European Union) strongly advise financial institutions to adopt a "human-in-the-loop" approach. In this model, AI serves only as a decision-support tool, while all investment execution must be reviewed and approved by qualified professionals.

Key Considerations Before Deploying AI In Wealth Management

Before deploying AI in wealth management, firms must carefully evaluate several critical factors to ensure performance, transparency, and regulatory compliance. Below are three key considerations that should be assessed before applying AI technologies.

Mitigating Bias In Algorithms

One of the biggest risks of using AI in wealth management is data bias. Since multimodal AI models learn from historical data, any imbalance in the training set can result in biased financial recommendations that disadvantage certain customer groups.

To ensure fairness, firms must conduct regular fairness testing and audits of AI algorithms. Using diverse datasets that represent different demographics, such as age, income level, and geographic region, helps prevent the model from favoring specific user segments.

Example:

A wealth management firm deployed an AI system to assess clients’ investment potential based on historical financial behavior. However, the training data mainly included urban clients aged 30–50 with high incomes.

As a result, the AI tended to recommend aggressive investment portfolios for this group while pushing low-yield, conservative products to younger clients (18–25) and those from rural areas.

Securing AI Systems Against Threats

AI systems in wealth management are increasingly becoming targets of cyber threats, including data breaches, model poisoning, and machine learning model theft. To mitigate these risks, firms must implement multi-layered security protocols.

These include data encryption, role-based access control, and secure authentication mechanisms. AI models should undergo regular security testing, such as penetration testing and threat modeling, specifically tailored for AI systems. Aligning AI operations with international cybersecurity standards—like ISO/IEC 27001—further ensures system integrity.

Prioritizing Explainability And Transparency

Many models function as a “black box,” meaning they make investment decisions without clearly showing the logic behind them. This can lead to mistrust from both financial advisors and clients, making it difficult to accept or act on AI-driven recommendations.

To address this, firms should adopt Explainable AI (XAI) tools that make AI decisions more transparent. Examples include LIME (Local Interpretable Model-agnostic Explanations) and SHAP (SHapley Additive exPlanations). These tools break down complex model predictions and explain why a certain investment suggestion was made.

How To Start Integrating AI Into Your Wealth Management Strategy?

Integrating artificial intelligence (AI) into wealth management is not merely a technology decision. Below are the fundamental steps for effectively embedding AI into your overall wealth management approach.

Define Your Objectives And Use Cases Clearly

The first step in integrating AI into wealth management is to define clear objectives. Firms must reassess their current challenges to identify which areas require improvement. From there, they can determine suitable and feasible AI use cases in wealth management that align with their existing systems and business goals.

Consider asking the following self-assessment questions:

- What is the primary goal of applying AI: driving revenue growth, enhancing personalized customer experience, or improving regulatory compliance?

- Where are the current bottlenecks: slow data analysis, manual advisory processes, or rising operational costs?

- Is there enough high-quality data to train the AI model?

- Is the data clean, unbiased, and representative?

- Which department should adopt AI first: investment management, client services, or internal operations?

For instance, a wealth management firm found its advisory team overwhelmed by the volume of mid-tier clients. After the assessment, the company chose to deploy a robo-advisor powered by artificial intelligence.

The AI system collects data from online questionnaires, financial histories, and spending behavior to automatically suggest preliminary investment portfolios based on each client’s risk profile.

Evaluate The Return On Investment And Risk Factors

Without proper oversight, implementing AI in wealth management can lead to significant risks in both cost and performance. Therefore, before scaling any initiative, businesses must conduct a thorough return on investment (ROI) analysis to ensure the value justifies the expense.

For example, a wealth management firm is considering developing an AI system to analyze and recommend personalized investment portfolios automatically. The estimated upfront cost is around VND 2 billion (approximately $80,000).

Currently, the firm employs three portfolio analysts with an annual operating cost of around VND 800 million per person. If the AI system can handle most of their workload without compromising performance, the company could save up to VND 2.4 billion annually. In this case, the business would recoup its investment in just 10 months.

Build A Culture Of Adoption And Training

To maximize the use of AI in wealth management, firms must shift their mindset from top-down the top. Employees should learn how to use AI tools and understand their role in decision-making processes. Training must include real-life scenarios to ensure practical application and build trust in the technology.

Effective ways to implement this include:

- Host internal simulation sessions: Recreate scenarios where AI suggests portfolio changes and financial advisors review and validate the decisions.

- Clarify specific use cases: For example, when AI recommends shifting to defensive assets, advisors should analyze the rationale before acting.

- Set clear expectations: Emphasize that AI supports, not replaces, human decision-making—especially in high-risk or compliance-sensitive situations.

- Encourage two-way feedback: Allow staff to question, challenge, and improve AI recommendations when outcomes seem off.

Start With Pilots And Scale Based On Results

Instead of rolling out full-scale deployments, firms should begin with small pilot projects. This enables them to validate the effectiveness of AI in wealth management while minimizing risk and adapting to real-world feedback.

Success should be measured using clear performance indicators such as cost savings, reduced response time, or increased revenue. These quantifiable outcomes help build internal confidence and secure continued investment in AI for asset management.

The Future Of AI In Wealth Management

The future of AI in wealth management is evolving rapidly, with a clear shift from assistive tools to autonomous and proactive systems. Below is a comprehensive outlook on how artificial intelligence is expected to transform the industry from multiple perspectives.

The Shift From Assistive To Autonomous And Proactive AI

In its early stages, AI in wealth management primarily served as an assistive tool for financial advisors, analyzing large datasets and recommending investment strategies. However, with evolving AI trends in wealth management, systems are now progressing toward autonomous and proactive AI.

This means AI can execute portfolio adjustments without direct human intervention, as long as it operates within predefined control parameters.

Example:

Mr. A, 35 years old, is a client of an AI-powered wealth management platform. He opts for a low-risk investment configuration, with the initial portfolio structured as follows:

- 60% in 5-year Vietnamese government bonds

- 30% in money market mutual funds

- 10% in stable blue-chip equities

On June 15, 2025, the government unexpectedly raised bond interest rates from 3.2% to 4.8% (announced by the State Treasury). This leads to a sharp 5% drop in bond prices on the secondary market.

AI-Driven Rebalancing Action:

- The AI system detects the risk level exceeding the acceptable threshold due to bond price volatility.

- It automatically sells 5% of the remaining bond allocation (accepting a small loss) and reallocates that portion into money market funds to stabilize the portfolio.

- After rebalancing, Mr. A’s new asset mix looks like this: 55% government bonds, 40% money market funds, 5% equities

- The system also sends a real-time notification to Mr. A

Will AI Replace Human Jobs And Disrupt The Labor Market?

A common concern in the financial industry is that artificial intelligence (AI) will replace human advisors, analysts, and customer service roles. According to Oxford & Frey (2013), approximately 47% of global jobs are at high risk of automation due to AI.

In wealth management, AI can automate technical tasks such as portfolio analysis, customer segmentation, and transaction processing. However, when it comes to emotional intelligence, ethical decision-making, or complex strategic thinking, human professionals remain essential.

This means that AI in wealth management will not entirely replace human talent but will shift the required skillsets. Statistics Canada reports that 31% of financial sector employees in Canada face a high risk of AI disruption, while another 29% are likely to benefit from it. These insights reflect broader AI trends in wealth management, where the technology serves as a performance enhancer rather than a complete substitute.

What Should Wealth Management Firms Do Today?

To keep up with emerging AI trends in wealth management, firms should not wait for artificial intelligence to become fully mature before taking action. Instead, they need a clear, proactive strategy that begins with:

- Training internal teams on AI technology and how it applies to financial operations.

- Identifying practical AI use cases in wealth management, such as analyzing client behavior or optimizing asset allocation.

- Investing in robust data infrastructure to ensure AI systems are efficient and secure.

- Staying updated with evolving legal and ethical frameworks surrounding AI for asset management.

Taking early action will give firms a competitive advantage as AI becomes an integral part of the wealth management industry.

Conclusion

AI is a strategic lever for wealth management firms looking to optimize performance, enhance client experience, and drive sustainable growth. If you're considering adopting AI in wealth management, start by defining clear objectives, piloting relevant AI use cases, and investing in a robust data infrastructure. Don’t miss the opportunity to future-proof your business in the era of digital transformation. Contact us now.

MOR SOFTWARE

Frequently Asked Questions (FAQs)

Is AI adoption in wealth management only for large firms?

No. Even small and mid-sized firms can leverage AI through scalable tools, cloud platforms, or fintech partnerships.

How can firms ensure AI decisions are ethical and transparent?

By using explainable AI models, establishing governance frameworks, and maintaining human oversight in critical processes.

Will clients trust AI-driven financial advice?

Yes, especially when advice is personalized, outcomes are transparent, and advisors remain involved in key decisions.

What’s the biggest barrier to adopting AI in wealth management?

The main challenges are often cultural: resistance to change, lack of AI-ready talent, and poor-quality or siloed data.

How do I measure the ROI of AI in wealth management?

Focus on tangible outcomes like better client retention, increased operational efficiency, improved investment performance, and advisor productivity.

Share

Rate this article

0

over 5.0 based on 0 reviews

Your rating on this news:

Name

*Email

*Write your comment

*Send your comment

1