13 Common Types of Payroll Fraud [How to Prevent Them]

Payroll fraud can hide in plain sight, inside timesheets, salary changes, benefits, reimbursements, or bank account updates. Left unchecked, it can drain money, damage trust, and create serious compliance risks. In this guide, MOR Software will explain the common types, red flags, real cases, and payroll fraud prevention steps businesses should know.

Key Takeaways

- Payroll fraud can happen through ghost employees, false timesheets, buddy punching, payroll diversion, duplicate payments, employee misclassification, unauthorized salary changes, inflated overtime claims, fraudulent expense reimbursements, benefits fraud, commission fraud, and payroll system manipulation.

- Strong approval flows, payroll audits, access control, and attendance checks help businesses spot payroll abuse before it grows.

- Better HRM, payroll, attendance, and finance system integration makes sensitive data easier to review and harder to misuse.

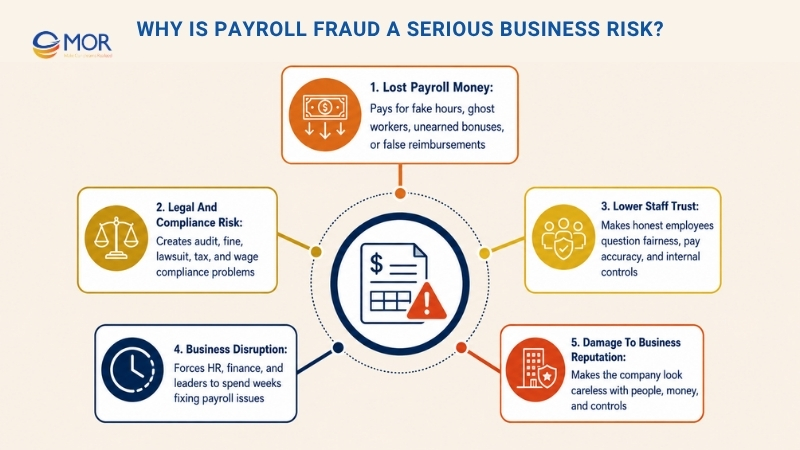

Why Is Payroll Fraud A Serious Business Risk?

Payroll fraud may seem like a small payroll mistake at first. Yet it can become a serious business threat because it drains cash, weakens trust, and may lead to legal or compliance trouble.

Industry research shows that payroll fraud affects 27% of companies and may cost an average of $383,000 for each case. The damage grows because these schemes can stay hidden for 18 to 30 months, giving losses time to pile up. Small and mid-sized companies face greater risk because they often have fewer tools, fewer checks, and less formal control than large firms.

In many cases, the problem begins with something that looks harmless, like extra overtime, a false claim, or one pay change without approval. But when the same actions continue across several payroll cycles, they can lead to large financial loss, legal risk, business disruption, and payroll fraud punishment in serious cases.

Lost Payroll Money

A company may pay for time no one worked, people who are not real employees, unearned bonuses, or fake reimbursements. For businesses with many workers, shift teams, or manual payroll steps, the loss can build fast before anyone sees the pattern.

Legal And Compliance Risk

When false payroll records, worker misclassification, tax errors, or unapproved wage changes go unchecked, the company may face audits, fines, lawsuits, or government reviews. Even if one worker caused the issue, the business may still need to prove that its controls, records, approval flow, and duty of care were strong enough.

Lower Staff Trust

Payroll feels personal because employees expect fair and correct pay. When staff learn that someone changed timesheets, added fake workers, or received unfair money, they may feel angry and lose trust. Honest workers may think the system protects bad behavior, which can hurt morale and daily work.

Business Disruption

HR, finance, accounting, and leaders may spend weeks reviewing reports, checking staff files, gathering proof, fixing payments, and improving controls. That time could have gone to growth plans, workforce planning, employee support, and other core tasks.

Damage To Business Reputation

If employees, customers, partners, or investors hear about the issue, they may question how well the company manages people and money. Weak payroll controls can make a business look careless, messy, or risky to work with. That is why stopping this problem is not only a finance task. It also protects business stability, employee trust, and long-term credibility.

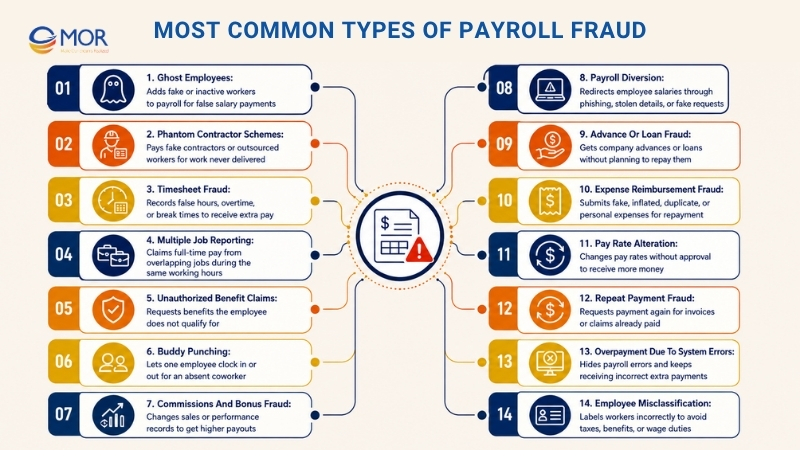

Most Common Types Of Payroll Fraud

Fraudulent payroll activity can take many forms, from fake workers and false timesheets to changed bonuses or stolen salary payments. These payroll fraud schemes are the main types every business should watch closely.

Ghost Employees

Ghost employee fraud takes place when someone adds a fake worker to payroll or leaves a former worker active after they have left. The person behind the scheme then receives wages for someone who does not really work for the company, making this one of the clearest forms of payroll fraud.

Example: A payroll staff member creates a fake employee account with a made-up name and bank account, then approves salary payments to that account each month.

Phantom Contractor Schemes

Phantom contractor schemes work much like ghost employee fraud, but they involve freelancers, outsourced staff, or temporary contractors. The company pays contractors who do not exist or who never delivered real work. In some cases, this payroll fraud may also link to money laundering.

Example: A manager approves bills from a fake IT contractor and sends the money to an account controlled by the person running the scheme.

Timesheet Fraud

Timesheet fraud happens when workers record more hours than they actually worked. This can include extra hours, unapproved overtime, or break times that are not recorded correctly. It is a common form of payroll fraud by employee because the false claim often starts inside the team.

Example: An employee leaves work at 5 PM but enters 7 PM as the end time to receive two extra hours of pay.

Multiple Job Reporting

Multiple job reporting happens when an employee claims to work full-time for more than one employer during the same working hours. Since the person cannot complete both jobs honestly at the same time, this creates false pay claims across more than one company.

Example: A remote employee accepts two full-time jobs with overlapping hours and reports full workdays to both employers.

Unauthorized Benefit Claims

Unauthorized benefit claims happen when employees ask for benefits they do not qualify for. Payroll fraud of this kind can raise total pay in an unfair way and create direct loss for the company.

Example: An employee claims a housing allowance or dependent support even though they do not meet the company’s rules.

Buddy Punching

Buddy punching occurs when one employee clocks in or out for another person. This lets a late or absent worker look like they completed a full shift. It is a simple type of payroll fraud, but it can cause large losses in shift-based teams.

Example: An employee asks a coworker to clock them in at 8 AM, even though they only arrive at 9:30 AM.

Commissions And Bonus Fraud

Commission and bonus fraud involves changing sales numbers, performance results, or achievement records to get higher payouts. Employees, managers, or companies may use this type of wage-related fraud to make results look better than they really are.

Example: A salesperson enters fake sales orders near month-end to qualify for a larger commission or bonus.

Payroll Diversion

Payroll diversion occurs when criminals use phishing, social tricks, or stolen personal details to send an employee’s salary to another bank account. This payroll fraud often targets HR or payroll teams because they handle salary and bank details.

Example: A scammer sends an email pretending to be an employee and asks HR to change the employee’s bank account before the next pay run.

Advance Or Loan Fraud

Advance or loan fraud happens when workers request salary advances or company loans with no plan to pay the money back. In some cases, they leave the company shortly after receiving the funds.

Example: An employee asks for a salary advance due to a personal problem, then resigns before repayment starts.

Expense Reimbursement Fraud

Expense reimbursement fraud happens when employees or businesses submit fake, inflated, or duplicate expense claims to receive money they should not get. Some companies may also misuse expense reports to lower tax duties, which can move into payroll tax fraud.

Example: An employee submits a personal dinner receipt and labels it as a client meeting cost.

Pay Rate Alteration

Pay rate alteration happens when an employee, contractor, or payroll user changes a pay rate without approval. This type of payroll fraud can cause the company to pay more than the person should receive.

Example: A contractor changes their hourly rate in the payroll system from $30 to $45 before invoices are processed.

Repeat Payment Fraud

Repeat payment fraud occurs when vendors, employees, or contractors ask for money for invoices, bills, or claims that were already paid. It may be done on purpose or hidden inside weak payment tracking.

Example: A contractor sends the same invoice twice with a slightly changed file name, hoping finance will pay it again.

Overpayment Due To System Errors

Overpayment due to system errors happens when payroll software, data entry mistakes, or system faults cause employees to receive more money than they should. It becomes fraud when the employee sees the mistake but hides it or keeps taking advantage of it.

Example: A payroll system applies overtime rates to normal working hours by mistake, and the employee stays silent after receiving several higher payments.

Employee Misclassification

Employee misclassification happens when a company labels workers incorrectly, often as contractors instead of employees. Some employer payroll frauds use this method to avoid overtime pay, benefits, payroll taxes, or legal duties linked to full-time staff.

Example: A business treats full-time workers as independent contractors even though they follow fixed schedules, use company tools, and work under direct company control.

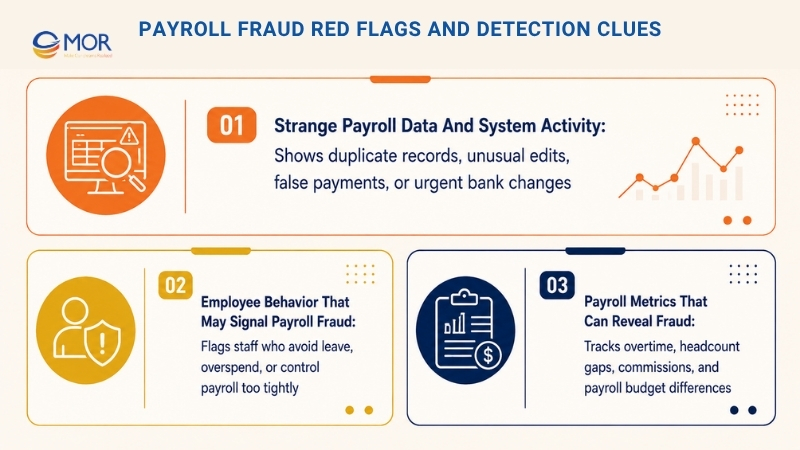

Payroll Fraud Red Flags And Detection Clues

Finding suspicious payroll activity early can save your business a lot of money. The sooner unusual payroll patterns are identified, the easier it is to limit financial losses, reduce disruption, and prevent small issues from turning into larger problems. Regular monitoring, clear approval processes, and timely reviews can help businesses detect suspicious activity before it causes significant damage.

Knowing the warning signs can make a real difference. These clues deserve quick attention during any payroll fraud investigation.

Strange Payroll Data And System Activity

Your payroll system can show many warning signs when you know what to check. Duplicate records, including shared bank accounts, Social Security numbers, addresses, or phone numbers, should raise concern. Payments made to former staff or people not found in active employee files also need review.

Repeated pay rate changes, time changes, or edits made without approval can also point to trouble. Be careful with payroll records that use very neat numbers, like exactly 10 or 20 overtime hours, because real working time is rarely that perfect.

Direct deposit changes need extra care. Fraudsters often send urgent emails that look like they came from employees and ask for quick bank account updates. Always confirm the request with the employee through the phone number already stored in your HR records.

Employee Behavior That May Signal Payroll Fraud

Some warning signs appear in how people behave at work. Employees who never take time off, or workers who suddenly spend far more than usual, may need closer review. Supervisors who demand full control over payroll tasks or approve their own timecards should also be watched carefully.

Payroll Metrics That Can Reveal Fraud

The numbers often speak before the problem becomes obvious. Track budget gaps, unusual overtime, paychecks that exceed active headcount, and commissions that do not match real sales. These gaps often point to payroll fraud or other internal misconduct.

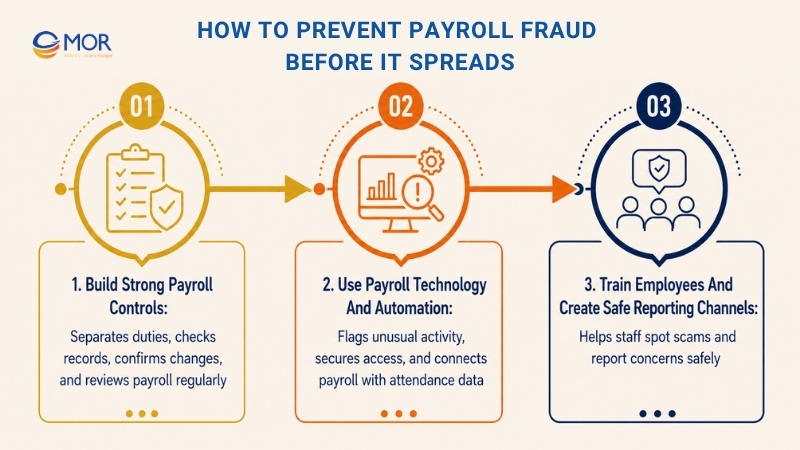

How To Prevent Payroll Fraud Before It Spreads

Businesses that act early often lose far less money to internal fraud. If you want to know how to prevent payroll fraud, the best place to start is with clear controls, clean records, and regular checks.

Build Strong Payroll Controls

Start with a clear split of payroll duties. One person can prepare payroll, another can approve new hires or pay changes, and a different person can review the final payment file. This setup keeps one employee from controlling the whole process, which makes dishonest activity harder to hide.

Give payroll system access only to people who need it for their role, and change passwords as soon as payroll staff leave. Ask managers to approve all payroll record updates, including salary changes, terminations, and bank account edits. For direct deposit updates, call the employee using the phone number already saved in your HR system. This simple check can prevent payroll fraud linked to salary diversion scams.

Monthly reconciliation is one of the best ways to catch gaps. Match payroll registers with bank statements, general ledger records, and tax forms like W-2s every month. Check if the number of active employees matches the number of issued payments. Run surprise checks on timesheets, commission payouts, and expense claims, preferably through someone outside the payroll team. Another smart control is asking payroll staff to take several days off in a row. As Accounting Today notes:

A worker who guards their tasks too closely and never takes PTO may be hiding fraud from anyone who could cover their work.

Fraud is often found when another employee steps in and sees something unusual.

Control Area | Action To Apply | Risk It Helps Stop |

Duty Split | Keep payroll preparation and approval separate | Fake wages, ghost employees |

Identity Check | Confirm direct deposit changes by phone | Payroll diversion and phishing |

Monthly Matching | Reconcile payroll with bank records each month | Payroll theft and unapproved checks |

Time Review | Match badge data against timesheets | Timesheet fraud and padded hours |

System Access | Use Multi-Factor Authentication (MFA) | Outside attacks and data breaches |

Strong controls give you the base, but technology can take payroll fraud prevention much further.

Use Payroll Technology And Automation

Technology helps teams move from late discovery to early warning. AI tools can flag odd behavior, including sudden overtime spikes, unapproved bonuses, or employee logins at strange hours. Some systems can find fraud within three months in 89% of cases, compared with 30 months when the issue is found by accident.

Digital timekeeping tools connected with payroll software can cut manual errors and reduce buddy punching. Biometric checks, including fingerprint scans or ID cards, help confirm the right employee is clocking in. Modern payroll tools also keep audit logs, which are useful when teams need to review unapproved changes.

Protect payroll data with Single Sign-On (SSO) and Role-Based Access Control (RBAC). Automated reconciliation tools can compare payroll accounts with bank records and flag unclaimed checks, timing gaps, or unknown transactions. When reviewing payroll software, look for standards like ISO/IEC 27001, SOC 2/SOC 3, and GDPR/CCPA compliance.

Technology helps a lot, but people still need to know what to watch for.

Train Employees And Create Safe Reporting Channels

Your employees can be the first people to notice suspicious activity. Train them to spot common scams like phishing, W-2 scams, and payroll diversion, where criminals pretend to be workers and ask for direct deposit changes. Remind staff not to share payroll or timekeeping login details with anyone.

Build a culture where people can raise concerns without fear. Give employees more than one way to report payroll fraud, including a manager they trust, an anonymous hotline, or outside bodies like the State Attorney General’s office or the FBI. Tips are the most common way fraud is found, making up 43% of cases. If someone suspects fraud, they should report it quietly so the person involved does not get time to hide or destroy records.

Train more than one person to handle payroll tasks so the business can keep running during leave or absence. This also gives the company a chance to find problems when another employee reviews the work. Small businesses face this risk more often than larger companies, so they gain a lot from these steps.

These actions protect payroll records and can also support business trust during funding rounds, lender reviews, or acquisition talks.

Payroll Fraud Vs Salary Fraud Vs Paycheck Fraud

These terms are often mixed together because they are related, but each one points to a slightly different type of wage-related misconduct:

Term | Meaning | Common Examples |

Payroll fraud | Payroll fraud is a wide type of employee fraud where payroll systems or records are changed to create payments that should not happen. | Ghost employees, timesheet fraud, buddy punching, paycheck diversion. |

Salary fraud | Salary fraud happens when someone gives false salary details to gain higher pay, better benefits, more work hours, or approval from a third party. | Inflated job titles, false salary details on a loan form. |

Paycheck fraud | Paycheck fraud means changing, stealing, or redirecting a single paycheck or payment method. | Forged checks, changed checks, redirected deposits, duplicate check cashing. |

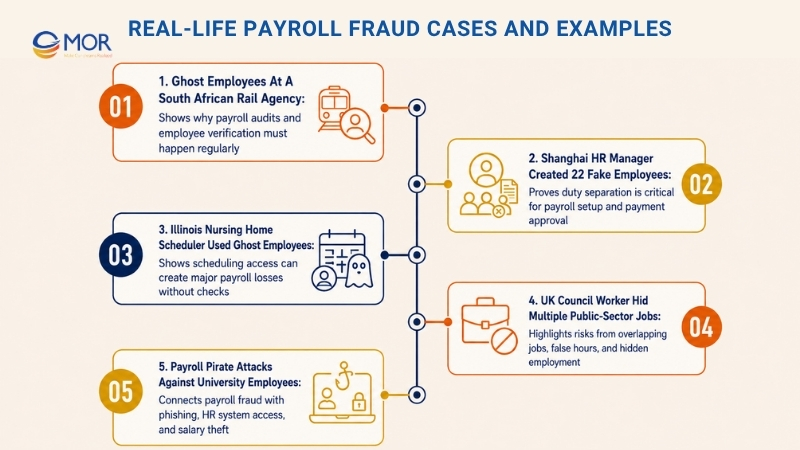

Real-Life Payroll Fraud Cases And Examples

Payroll fraud cases may sound like small accounting problems, but real incidents show how varied and serious they can be. Some involve one worker changing timesheets or sending wages to another bank account. Others involve payroll leaders adding fake employees, public workers hiding extra jobs, or hackers breaking into HR systems to steal salaries. These payroll frauds examples show that the issue often begins with poor controls, weak review steps, limited verification, or too much access in one person’s hands. Payroll fraud news also reminds businesses that this risk can appear in private firms, public bodies, healthcare, education, and large enterprises.

Ghost Employees At A South African Rail Agency

One well-known ghost employee case involved the Passenger Rail Agency of South Africa (PRASA). After problems were found in its ICT, human capital management, and payroll systems, PRASA began an employee verification project. The goal was to confirm that every worker listed in payroll was real, active, and properly recorded.

The project uncovered serious control gaps. Thousands of workers were asked to appear for in-person checks, but many could not be verified. Some resigned during the review, and others failed to provide proper documents. The findings raised concern that ghost workers had been added to payroll or that inactive employee records had not been removed.

This case shows how risky weak employee verification can be. When a company does not compare payroll files with HR records, ID documents, contracts, and active work data, ghost employees can stay hidden for a long time. In a large organization, even a small number of fake payroll entries can turn into heavy losses.

Business Lesson: Run payroll audits, verify employees, and compare payroll data with HR records on a regular schedule. Every person on payroll should have a confirmed identity, a valid work record, a named manager, and proof of real work.

Shanghai HR Manager Created 22 Fake Employees

Another major payroll embezzlement case took place in Shanghai, where an HR manager at a labor services company created false employee records to steal salary and severance money. He managed payroll for workers assigned to a technology company. Since he had too much control over placement records and salary payments, he could create fake workers and approve payments without proper review.

The scheme included 22 fake employees and led to millions of yuan being stolen from the business. It lasted because there was no strong approval flow, no separate payroll review, and no clear split between the person creating worker records and the person approving salary payments.

This case shows what can happen when one person owns too many payroll steps. The fake workers were only part of the issue. The bigger weakness was the lack of internal review, which allowed one HR employee to create the records, manage the process, and gain money from it.

Business Lesson: One employee should never control payroll setup, salary approval, and payment release at the same time. Companies need duty separation, approval flows, audit logs, and regular payroll reconciliation to lower insider fraud risk.

Illinois Nursing Home Scheduler Used Ghost Employees

In the United States, a former scheduler at an Illinois nursing and rehabilitation facility pleaded guilty to a ghost employee scheme. She was in charge of scheduling Certified Nursing Assistants, but used that access to make it look like several people worked at the facility when they did not.

She sent false timesheets and payroll records, which caused the facility to issue checks to ghost employees. In some cases, the money was shared with those people. In other cases, checks were signed over or deposited for personal use. The facility paid more than $100,000 for work that never happened.

This case matters because payroll fraud does not always need a senior leader or payroll manager. Someone with scheduling power, timekeeping access, or influence over payroll records can also create large losses when checks are weak.

Business Lesson: Payroll records should not depend on one person’s schedule or timesheet input. Companies should match timesheets with attendance logs, manager approvals, work assignments, and real staffing needs before payroll is processed.

UK Council Worker Hid Multiple Public-Sector Jobs

A UK council employee was found guilty of fraud after secretly holding several public-sector jobs at the same time. The worker received salaries from different organizations without properly sharing the overlapping employment. The case included false timesheets, misstated work hours, and public money paid for work that was not honestly reported.

This type of payroll abuse matters more now because remote and hybrid work can make it harder to check working time, availability, and output. When staff work for different organizations without disclosure, they may claim the same hours from more than one employer.

The case also shows that the worker does not always need to be fake. Sometimes the person is real, but their hours, availability, and work claims are false. This can be harder to find when employers do not review workloads, meeting attendance, deliverables, and payroll patterns.

Business Lesson: Employers need clear outside work policies, conflict-of-interest forms, manager checks, and data reviews that find unusual overlaps in work hours or pay claims.

Payroll Pirate Attacks Against University Employees

Payroll abuse is no longer only an internal HR or accounting problem. Cybercriminals now use phishing and business email compromise tactics to enter payroll and HR systems. In one campaign reported by Microsoft, a financially driven threat actor targeted university employees to access HR software profiles and redirect wages to bank accounts controlled by attackers.

The attackers sent phishing emails to steal login details and multi-factor codes. After entering an employee account, they opened HR profiles, changed payroll payment settings, and created inbox rules that hid warning emails about the payroll edits. This made the scheme harder for the employee and the organization to spot quickly.

This case shows how wage theft and cybersecurity now connect. Even with correct payroll records, attackers can still steal salaries if they access employee accounts, HR platforms, or direct deposit settings.

Business Lesson: Payroll security should include phishing-resistant MFA, direct deposit change checks, login monitoring, employee training, and alerts for suspicious payroll profile updates.

How MOR Software Helps Reduce Payroll Fraud Risk With Better Systems

Payroll fraud often happens when HR, payroll, attendance, and finance data sit in separate places. One team checks working hours. Another team updates salary records. Finance processes payment. When the system depends too much on manual work, small changes can pass without review.

MOR Software helps businesses build safer HRM, payroll management system, attendance, and integration systems that make payroll data easier to check and harder to abuse.

- Build custom HRM and payroll systems: MOR Software can develop systems for employee records, time attendance, payroll, leave management system, benefits, overtime, bonus, reimbursement, and approval flows. This gives HR and finance teams one clear place to manage sensitive payroll data.

- Connect payroll with attendance and HR data: MOR Software can link payroll with HRM, time attendance, ERP, CRM, Salesforce, Slack, or legacy systems. This helps teams cut manual data entry and lowers the risk of errors, duplicate records, or missing updates.

- Create approval workflows: Businesses can set clear approval steps for salary changes, overtime, bank account updates, bonus payments, and reimbursement claims. Each request can go through the right manager before it reaches payroll.

- Add audit trails and access control: A safer payroll system should record who changed data, what changed, and when the change happened. MOR Software can add role-based access, change history, and permission settings so sensitive records are not open to everyone.

- Use automation to detect unusual patterns: The system can flag overtime spikes, duplicate bank accounts, inactive employees still receiving pay, or payroll changes made outside the normal process. These alerts help teams review payroll fraud risks before they grow.

- Modernize legacy payroll systems: Many businesses still rely on old tools, Excel files, or disconnected internal systems. MOR Software can help rebuild or connect these systems so payroll records are easier to check, audit, and manage.

MOR Software does not replace legal, audit, or fraud investigation teams. Its role is to help businesses build the right software foundation. When payroll data, HR records, attendance logs, and approval steps work together, fraud has fewer places to hide.

Conclusion

Payroll fraud is hard to catch when payroll data sits across disconnected tools and manual files. The best defense starts with clear controls, clean records, smart alerts, and safe reporting channels. Businesses also need systems that connect HR, attendance, payroll, and finance data in one trusted flow. MOR Software helps companies build custom HRM, payroll, and integration systems that make fraud risk easier to see, check, and manage. Contact MOR Software to discuss your payroll system needs.

"Solutions Director at MOR Software, has extensive expertise in software development and management. He leads innovative projects and provides strategic solutions to enhance business operations, helping clients achieve digital transformation goals."

Pham Huu Canh

Solutions Director

MOR SOFTWARE

Frequently Asked Questions (FAQs)

What is payroll fraud?

Payroll fraud happens when someone abuses a company’s payroll process to receive money they should not get. It may involve fake employees, false hours, unapproved overtime, salary changes, or redirected payments.

What are the most common payroll scams?

Common scams include ghost employees, timesheet padding, buddy punching, fake contractors, false reimbursement claims, bonus manipulation, and direct deposit changes made without approval.

Who can commit this type of fraud?

It can come from employees, payroll staff, HR teams, managers, contractors, or outside attackers. In some cases, insiders and outsiders work together to change records or move payments.

Why are small businesses at higher risk?

Small businesses often have fewer people checking payroll records. One person may handle employee data, approvals, and payments. That makes false records harder to spot.

What are the warning signs in payroll records?

Watch for duplicate bank accounts, repeated overtime, payments to inactive employees, sudden pay rate changes, or payroll entries with round numbers. These clues may point to a deeper issue.

How can a company prevent fake employees?

Companies should verify every worker’s identity, contract, manager, role, and work record. Payroll lists should also be compared with HR records and attendance data on a regular schedule.

How can businesses stop timesheet abuse?

Use digital timekeeping, manager approvals, attendance checks, and random audits. For shift-based teams, compare clock-in data with schedules and actual staffing needs before payroll is processed.

Why are direct deposit changes risky?

Attackers may impersonate employees and ask payroll teams to send wages to a new bank account. Every bank change should be confirmed through a trusted contact method already stored in HR records.

What role does technology play in prevention?

Payroll systems can flag odd patterns faster than manual checks. Alerts can catch duplicate accounts, unusual overtime, inactive workers still being paid, or changes made outside the normal workflow.

What should a business do if it suspects a problem?

The business should limit access, preserve records, review payroll data, and involve HR, finance, legal, or audit teams. Staff should report concerns quietly so records are not changed or deleted.

Share

Rate this article

0

over 5.0 based on 0 reviews

Your rating on this news:

Name

*Email

*Write your comment

*Send your comment

1