What Are Payroll Deductions and How to Calculate Them Accurately?

Understanding what are payroll deductions is a headache for many businesses, especially when mistakes can lead to fines or unhappy employees. From taxes to benefit contributions, the rules can feel overwhelming. In this guide, MOR Software will break down the basics of payroll deduction meaning and show you how to calculate them accurately.

What Are Payroll Deductions?

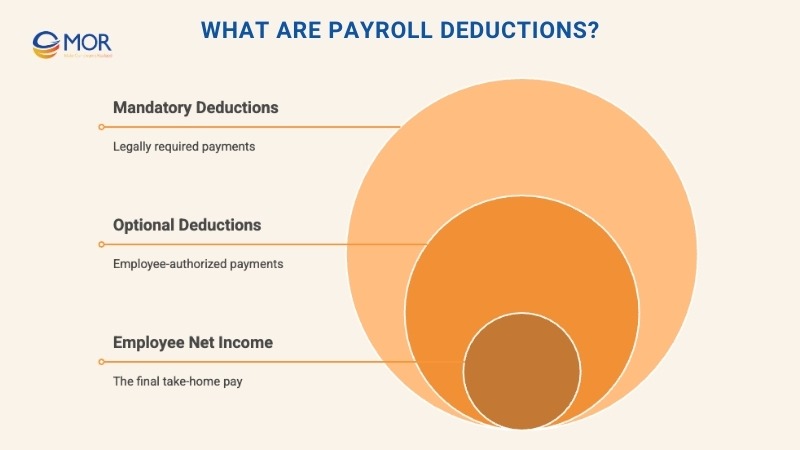

What are payroll deductions? In simple terms, they are amounts taken from an employee’s gross wages to cover required or approved payments. These deductions explain the gap between total earnings and the net amount that employees actually take home.

In the United States, common items withheld include:

- Federal and state income tax

- Social Security contributions

- Medicare contributions

- Retirement savings, such as 401(k) plans

- Court-ordered wage garnishments

- Child support obligations

Some employee deductions are optional and may occur on a pretax or post-tax basis if the worker signs an authorization form. Examples include health insurance or retirement contributions.

In March 2025, the U.S. Bureau of Labor Statistics reported that 72% of private-industry workers had access to retirement benefits. This means deductions tied to retirement plans still appear on many U.S. paychecks.

For health coverage, the 2025 KFF Employer Health Benefits Survey found that workers contributed an average of 6,850 dollars toward family coverage. In most cases, this amount is paid through payroll deductions.

Others, like taxes and wage garnishments, are mandatory. Employers must calculate them correctly, since failing to withhold the right amount can make the business responsible for unpaid sums.

This explains the payroll deduction meaning and shows how it directly shapes the difference between gross and net pay. For growing enterprises that find handling complex localized legalities too overwhelming, partnering with specialized payroll outsourcing companies can offload the administrative burden entirely.

How Do Payroll Deductions Work?

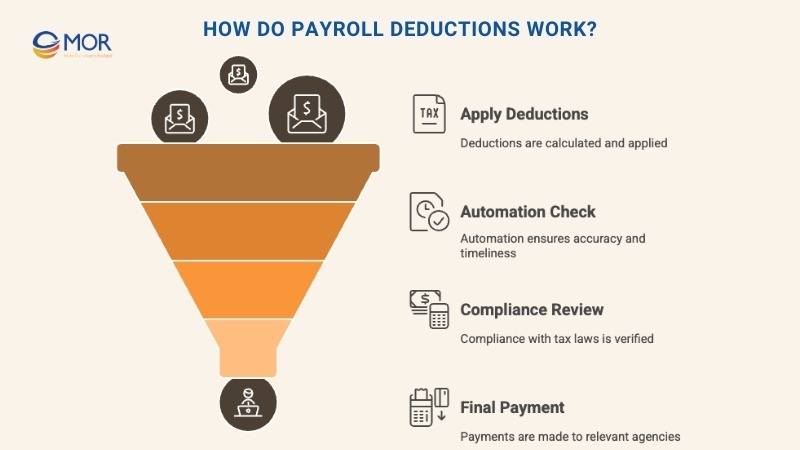

What are the payroll deductions in practice? In the U.S., they are handled every pay cycle, following federal, state, local, benefit plan, or court requirements. Employers can run the numbers by hand or rely on a payroll system that automates calculations.

Many companies prefer automation, since it lowers mistakes and helps money reach the right tax agencies, benefit providers, or courts on time. In FY 2023, 70% of all child support collections were obtained through income withholding from paychecks. This shows how central employer processing is to court-ordered deductions.

The exact amount taken from each paycheck depends on several details. The employee’s Form W-4, state or local withholding certificates, chosen benefits, and any court-ordered deduction payroll items all come into play.

For example, someone enrolled in the company’s health plan will see those costs deducted, while another employee may have garnishments that must be withheld.

Location also matters. In the U.S., where a business operates and where its staff members work can affect deductions, since not every state requires income tax. In 2026, some states still have no broad wage-based state income tax, so employees there follow different state withholding rules.

This makes understanding what are deductions on a paycheck important for accurate records and compliance.

Payroll Deduction Rules Change By Country

There is no single global formula for payroll deductions. The theory is similar everywhere: employers withhold part of gross pay for tax, social insurance, benefit plans, or approved employee payments. Yet each country decides its own rates, exemptions, forms, limits, and reporting rules.

This guide uses the U.S. payroll system as the main reference, including federal income tax, FICA taxes, state tax rules, 401(k) contributions, and wage garnishments. Other countries calculate payroll deductions differently, so employers should always check local rules before applying any formula.

In the U.S., payroll deductions often include federal income tax, FICA taxes, state income tax, health insurance premiums, 401(k) contributions, and wage garnishments. Employers use IRS guidance, Form W-4 details, state tax guides, and benefit plan rules.

In Vietnam, salary payroll often involves personal income tax, compulsory social insurance, health insurance, unemployment insurance, and family-based tax relief rules. The taxable income calculation is not the same as the U.S. model.

In Australia, employers usually deal with PAYG withholding, superannuation guarantee rules, and salary sacrifice arrangements. These do not match U.S. payroll terms like FICA or 401(k).

This is why this article uses the U.S. as the main example. If your company hires in more than one country, the payroll system must support country-specific deduction rules instead of forcing one fixed setup across every market.

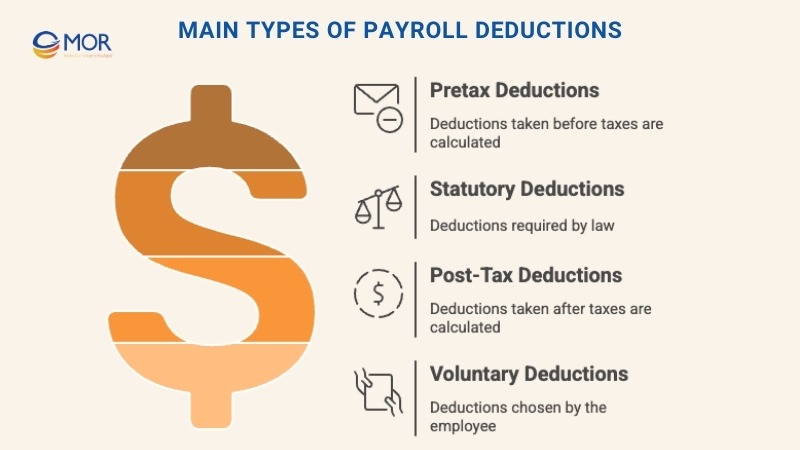

Main Types Of Payroll Deductions

Understanding what are payroll deductions isn’t complete without knowing the categories they fall into. We’ve broken down the main types so you can see how each affects employee pay and compliance in the U.S.

Pretax Deductions

Pretax deductions come out of an employee’s pay before certain taxes are applied. Since these amounts are removed from gross wages first, they can reduce taxable income and lower the tax bill owed to the government.

Common pretax deductions for payroll include health insurance premiums, certain retirement contributions, and group-term life insurance under approved plans.

Participation is optional, but many employees choose it because pretax contributions usually cost less than paying for the same benefits after taxes. These deductions directly shape the payroll meaning for both employers and workers.

There are limits, though. Federal rules set annual contribution caps on certain pretax benefits. For example, the IRS sets a maximum on how much an employee can defer each year into a 401(k) retirement plan. Staying within these caps is necessary to keep the pretax benefit.

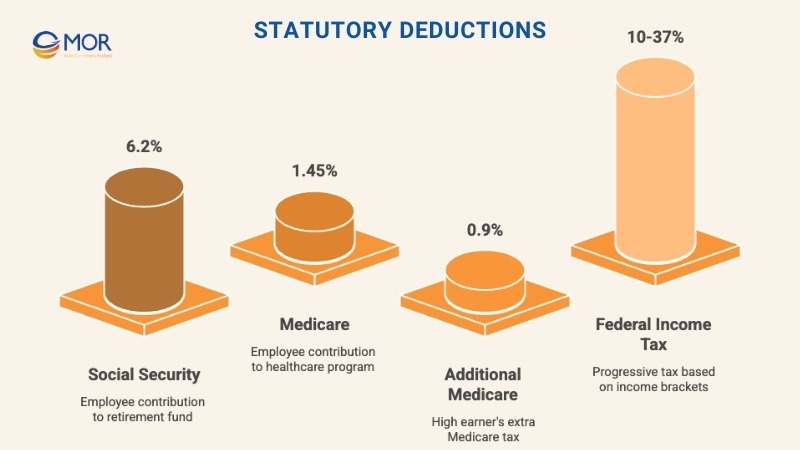

Statutory Deductions

Statutory deductions are required by law and fund government programs. In the U.S., they commonly cover federal income tax, state income tax, and the Federal Insurance Contributions Act (FICA) tax, which supports Medicare and Social Security.

To calculate them correctly, employers must confirm each worker’s employment classification.

For independent contractors, you typically don’t withhold income tax, Social Security, or Medicare, since contractors pay self-employment tax themselves. In contrast, when the worker is classified as a direct employee, you must withhold and submit the proper taxes.

If there’s uncertainty about classification, employers can request guidance by filing Form SS-8 with the IRS. These rules show how employer taxes connect directly to lawful deductions for payroll.

FICA Taxes

FICA taxes cover contributions to Social Security and Medicare. For 2026, each U.S. employee pays 6.2% toward Social Security, up to the annual wage limit of 184,500 dollars, and 1.45% for Medicare with no wage cap.

Together, this makes 7.65% taken out of every paycheck until the Social Security wage base is reached. Employers must match this same amount, making FICA a shared payroll tax cost.

High earners may also owe the Additional Medicare Tax. Once wages go above 200,000 dollars in a calendar year, an extra 0.9% must be withheld from that point forward.

Unlike standard FICA, employers don’t have to match this deduction payroll item. This is a key part of the broader payroll tax system that keeps public programs funded.

Federal Income Tax

The U.S. federal income tax system uses seven brackets, starting at 10% and reaching up to 37%. These rates are progressive, so employee wages are taxed in layers. Income is first charged at the lowest rate, then moves upward through higher brackets.

The exact taxable income ranges in each bracket depend on filing status, such as single, married filing jointly, married filing separately, or head of household. These details are reflected through Form W-4.

Each year, the IRS adjusts many tax thresholds for inflation, which can shift where employees fall.

For withholding, employers usually use either the wage bracket method or the percentage method. Both options are explained in IRS Publication 15-T and guide employers in applying this core part of employee deductions during each pay cycle.

State and Local Taxes

Rules for state income tax differ across the U.S. A number of states use a flat rate on all income, some apply several tax brackets, and a handful collect no broad wage-based income tax at all.

Some cities and local governments may also require income tax withholding. Because of this variety, employers must review the laws in every state and local area where staff members work to keep paid payroll in line with local requirements.

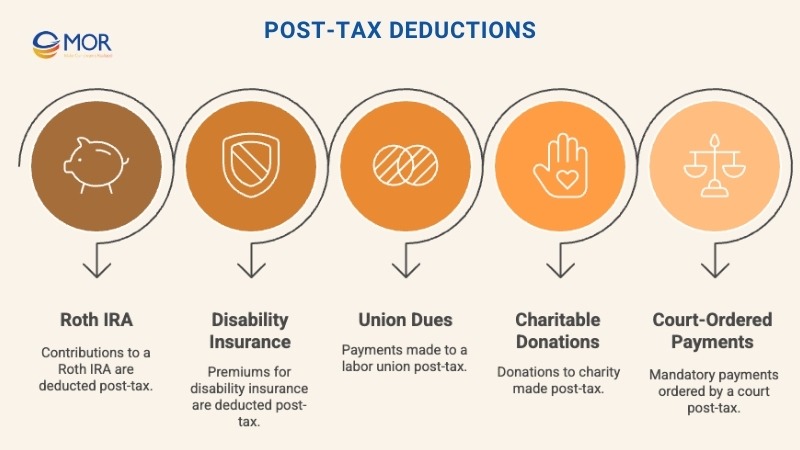

Post-Tax Deductions

Post-tax deductions come out of wages after mandatory taxes are withheld. Since they are taken from net pay instead of gross pay, they usually don’t lower taxable income.

Examples include Roth IRA contributions, disability insurance premiums, union dues, charitable donations, and court-ordered payments. Employees may opt out of most post-tax items, but wage garnishments are not optional.

These deductions are an important part of understanding the full payroll deduction meaning for employees.

Wage Garnishments

A court, government agency, or the IRS can order you to withhold part of an employee’s wages to repay debts like unpaid taxes, child support, alimony, or defaulted loans.

Garnishment can apply to:

- Hourly pay

- Salaries

- Commissions

- Bonuses

- Pension or retirement plan payments

Each garnishment order will state the exact amount or percentage to withhold and where the funds should be sent. Employers must review these documents closely. Errors in calculation or failure to send payment may leave the business liable for unpaid amounts.

On top of the order itself, employers must also comply with Title III of the Consumer Credit Protection Act (CCPA). This law sets limits on how much of an employee’s wages can be garnished in a week and protects employees from being terminated solely because of one garnishment.

This highlights why accurate handling of such deductions for payroll matters.

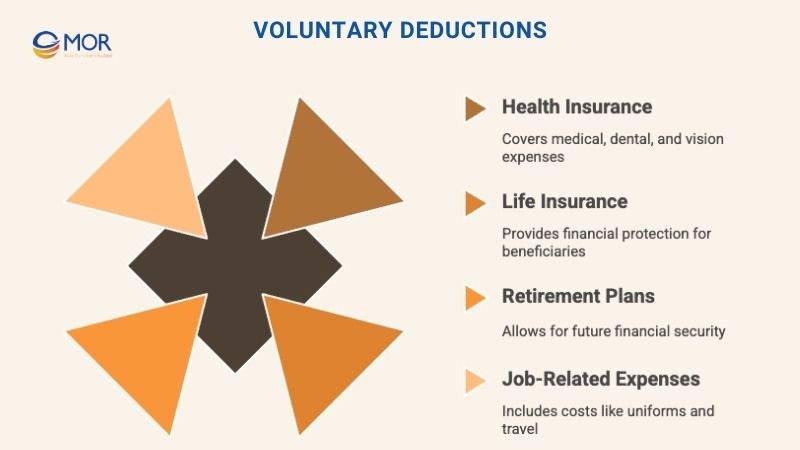

Voluntary Deductions

Voluntary deductions are amounts employees agree to have withheld from their paychecks to cover benefits or other services. These can be taken out on a pretax basis under Section 125 of the Internal Revenue Code, or after tax depending on the type of benefit.

Since these deductions are optional, employers must be clear and transparent. Always obtain written consent before deducting insurance premiums, retirement contributions, or similar items.

Each pay statement should show the current deduction and the year-to-date total. Accurate records matter, and many states require this reporting by law.

Common types of voluntary deduction payroll include:

Health Insurance

Providing medical, dental, and vision coverage helps employers attract and keep skilled staff. To avoid the expense becoming a bigger burden, many businesses handle premiums on a pretax basis.

Doing so is often more cost-effective for both employer and employee, but the IRS requires that pretax contributions follow a Section 125 plan.

Group-Term Life Insurance

Many employers provide basic term life insurance at no cost to employees, often up to 50,000 dollars of coverage. Any employer-paid coverage above that threshold is generally treated as taxable income.

When employees choose to add extra coverage or extend policies to their dependents, the additional premium is normally withheld from pay on a post-tax basis. These arrangements fall under voluntary deductions for payroll and must be recorded clearly on pay statements.

Retirement Plans

Retirement savings plans are another common form of employee deductions. In the U.S., 401(k) plans and Roth retirement accounts are among the most common.

Traditional 401(k) contributions are usually deducted before federal income tax. Yet they remain subject to Social Security and Medicare taxes.

Roth contributions work differently. They are deducted after tax, meaning employees pay taxes upfront but may receive tax-free withdrawals in retirement if they meet the plan rules.

Both options play an important role in long-term financial planning.

Job-Related Expenses

Union employees often see deductions for membership fees along with any taxable benefits provided by the union. Other common work-related costs that may appear in payroll include uniforms, meal plans, tools, or travel-related costs.

Still, not every state permits these types of withholdings. Some states restrict deductions that could bring pay below minimum wage or shift business costs to employees.

Employers need to check local laws before applying such deduction payroll items.

>>> Let's highlight the top HRMS payroll software picks for 2026, explain how these systems work, and help you choose a solution that truly fits your business.

Payroll Deduction Authorization Form

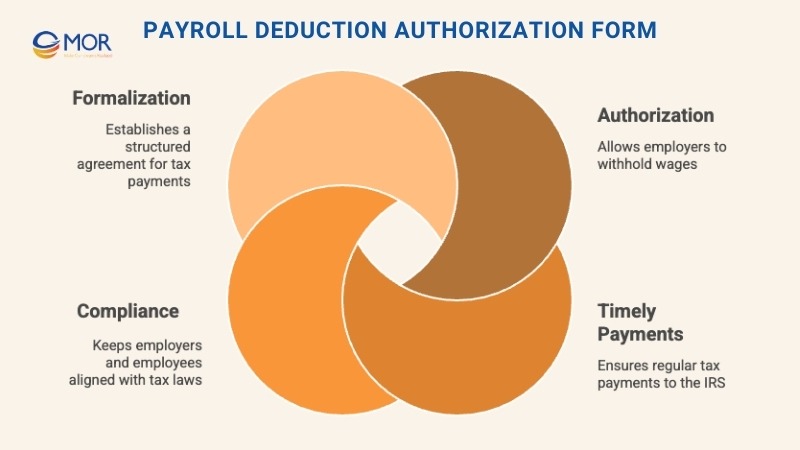

Employers may use IRS Form 2159, Payroll Deduction Agreement, when an employee owes back taxes. This document notifies the IRS that a portion of the employee’s wages will be withheld and sent directly to the government.

It also confirms the payment schedule, helping the employer submit funds on time and in line with the agreed frequency. This process formalizes the arrangement and keeps both parties aligned with federal payroll tax requirements.

For voluntary deductions, employers should also keep written employee authorization. This may include benefit enrollment forms, retirement plan elections, or signed payroll deduction forms.

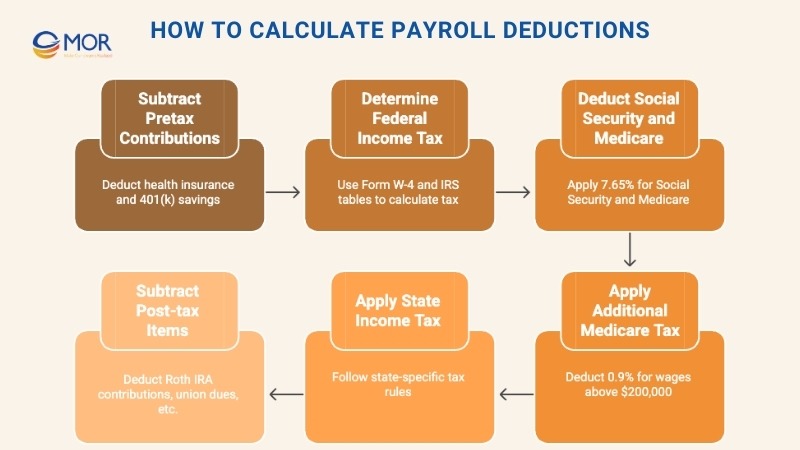

How to Calculate Payroll Deductions

The process of calculating what are payroll deductions means converting an employee’s gross pay into their final net pay. In a U.S. payroll setting, employers usually follow these steps:

- Start with gross wages for the pay period.

- Subtract pretax contributions, such as Section 125 health insurance premiums, 401(k) savings for income tax purposes, and other approved voluntary benefits.

- Use the employee’s Form W-4 and IRS withholding tables to determine federal income tax withholding.

- Deduct Social Security and Medicare taxes under FICA rules.

- Apply the Additional Medicare Tax once annual wages exceed 200,000 dollars.

- For states or cities with income tax, follow the official state or local employer tax guide.

- Remove post-tax items like Roth contributions, union dues, charitable donations, or garnishments.

- Calculate net pay and record each deduction on the employee’s pay statement.

Employers often rely on payroll systems to automate these steps. This helps keep every payroll deduction meaning accurate and lowers the chance of costly mistakes. Compliance is key to sustainable growth. Read our definitive guide on building a robust payroll management system.

U.S. Payroll Deduction Example: A Single Employee With Health Care And 401(k)

Let’s look at a simple U.S. example. This case is only for illustration, since real payroll depends on Form W-4 details, state rules, benefit plans, and pay frequency.

Assume an employee:

- Works in the U.S. as a W-2 employee

- Earns 80,000 dollars per year

- Files as single

- Has no dependents

- Works in a state with no state income tax

- Pays 3,000 dollars per year for pretax health insurance

- Contributes 4,000 dollars per year to a traditional 401(k)

- Has no wage garnishment

- Does unpaid volunteer work on weekends, with no wages or taxable stipend

The unpaid volunteer work does not enter this payroll calculation because no wages are paid. If a nonprofit or employer pays a taxable stipend, that payment may need a separate review.

Here is a simplified annual calculation:

Payroll item | Amount |

Gross annual pay | $80,000 |

Pretax health insurance | -$3,000 |

Traditional 401(k) contribution | -$4,000 |

Federal income tax wages before standard deduction | $73,000 |

2026 standard deduction for single filer | -$16,100 |

Estimated taxable income | $56,900 |

Using 2026 federal tax brackets for a single filer, the estimated annual federal income tax would be:

- 10% on the first 12,400 dollars = 1,240 dollars

- 12% on the next 38,000 dollars = 4,560 dollars

- 22% on the remaining 6,500 dollars = 1,430 dollars

Estimated federal income tax: 7,230 dollars

For FICA, the health insurance premium may reduce Social Security and Medicare wages if it is part of a qualified Section 125 plan. Traditional 401(k) contributions usually do not reduce FICA wages.

FICA item | Calculation | Amount |

FICA wages | $80,000 - $3,000 | $77,000 |

Social Security | $77,000 × 6.2% | $4,774 |

Medicare | $77,000 × 1.45% | $1,116.50 |

Total FICA |

| $5,890.50 |

The employee’s estimated annual net pay would be:

80,000 - 3,000 - 4,000 - 7,230 - 5,890.50 = 59,879.50 dollars

Estimated monthly take-home pay would be about 4,990 dollars, before any other post-tax deductions.

This example shows why payroll deductions need a clear order. Pretax health insurance, 401(k), federal tax, FICA, and post-tax items do not all follow the same calculation base.

Simplify Your Payroll Deductions With MOR Software

For business owners, payroll deductions can be one of the most time-consuming and error-prone parts of managing a team. Tax rules change, benefits vary, and even small mistakes can lead to compliance headaches or unhappy employees. Manually calculating pre-tax and post-tax percentages is a leading cause of compliance errors, frequently resulting in catastrophic payroll mistakes that can damage employee trust.

MOR Software builds tailored payroll systems that automate every deduction step, from taxes to voluntary benefits. Our solutions cut down manual work, improve accuracy, and give you a clear view of payroll costs in real time.

With our expertise, you gain a reliable system that keeps your payroll deductions simple, compliant, and ready to grow with your business.

Conclusion

Knowing what are payroll deductions and how to calculate them correctly is essential for smooth payroll management. From statutory taxes to voluntary benefits, every deduction affects both compliance and employee satisfaction. Missteps can cost time, money, and trust.

With the right systems in place, you can turn a complicated process into a simple, transparent workflow. That’s where MOR Software comes in. We build payroll solutions that automate deductions for payroll, ensure compliance, and give you accurate records every time. Ready to simplify payroll and focus on growing your business? Contact us today to see how our expertise can support you.

"Solutions Director at MOR Software, has extensive expertise in software development and management. He leads innovative projects and provides strategic solutions to enhance business operations, helping clients achieve digital transformation goals."

Pham Huu Canh

Solutions Director

MOR SOFTWARE

Frequently Asked Questions (FAQs)

What is deducted from payroll?

Along with federal and state taxes like income tax and payroll taxes, employees may also see other amounts taken from their paycheck. Some of these are “pretax deductions,” which reduce taxable income. They often include retirement plan contributions and certain health care expenses.

What are the two types of deductions?

Deductions fall into two categories: standard and itemized. The standard deduction is a fixed amount based on filing status. If your deductible costs are higher than that amount, you can choose to itemize by listing each expense individually, which may reduce your taxable income more.

What is the most common deduction from your paycheck?

The most frequent payroll deductions are federal income tax, state income tax, Social Security, and Medicare. Other possible deductions include health insurance premiums, retirement contributions, and wage garnishments.

How do you record payroll deductions?

When making the journal entry, you record the total gross pay as a debit to wage expense. Then, debit payroll tax expenses and credit liability accounts for each deduction. Finally, credit the cash account for the net amount actually paid to employees.

What does it mean to deduct your salary?

A salary deduction is money taken from an employee’s gross pay before calculating net pay. These deductions can include taxes, retirement contributions, insurance premiums, and other approved expenses.

What are some examples of deduction?

Deductive reasoning follows a rule where if the starting statements are true, the conclusion must also be true. For instance, “All dogs have ears. Golden retrievers are dogs. Therefore, golden retrievers have ears.” Another example: “All racing cars can exceed 80 MPH. The Dodge Charger is a racing car. So, it can go over 80 MPH.”

How do deductions work?

Deductions reduce your taxable income, meaning you pay tax on a smaller amount. Tax credits, on the other hand, directly lower the amount of tax you owe. Some credits are refundable, which means if they lower your tax below zero, you receive the extra as a refund.

What are the deductions allowed in income tax?

Commonly allowed deductions include life insurance premiums, contributions to PPF, repayment of home loan principal, investments in ELSS funds, and deposits into schemes like Sukanya Samriddhi Yojana. Using these deductions wisely can help reduce your tax bill under Section 80C.

What is a 100% deduction?

Expenses that are fully deductible (100%) include holiday parties, meals at open houses, and some business-essential meals. Others, like client meals or in-office meeting meals, may be only 50% deductible. Entertainment costs, such as sports tickets or club memberships, are usually not deductible at all.

Share

Rate this article

0

over 5.0 based on 0 reviews

Your rating on this news:

Name

*Email

*Write your comment

*Send your comment

1