How to Create a Digital Wallet: Step-by-step Guide for Business

Learning how to create a digital wallet can feel risky when payments, user trust, security, KYC, and app costs all sit on the same table. One weak login flow or poor payment gateway choice can hurt adoption fast. This MOR Software’s guide walks through the full digital wallet development process, from wallet types and core features to security, cost, and launch planning.

What Is A Digital Wallet?

A digital wallet is an app that keeps your cards, IDs, passes, and tickets on a phone, tablet, or computer. You can pay in a store with a tap or buy online without entering card details again and again.

Think of it as a wallet that lives inside your device. Instead of carrying cards, you keep the main payment tools in one protected app.

Modern mobile wallet app work is built around this smooth and simple payment flow. For businesses learning how to create a digital wallet, ease of use should come before extra tools.

Some well-known digital wallets include:

- Apple Pay

- Google Pay

- PayPal

- Venmo

- Samsung Pay

These products prove a simple point. When you build a fintech app or create a digital wallet, users care more about a clean flow than a long list of complex tools.

Why Secure Digital Wallet Development Matters In 2026

According to McKinsey, U.S. in-store digital wallet use rose from 19% in 2019 to 28% in 2024. The same study found similar behavior across eight European countries. Even in cash-heavy markets like Germany and Italy, about 25% of users had paid in-store with a digital wallet during the past year.

The mobile wallet market reached $71.6 billion in 2024, and demand is still rising. For companies, that means a wallet platform is no longer a ‘nice extra’ as more customers expect fast mobile payments.

For teams learning how to create a digital wallet, the goal is simple. The product must feel easy, safe, and suited to the industry it serves.

What else can this kind of app do? Apart from P2P transfers and mobile payments, it can help users:

- save loyalty points;

- control subscriptions;

- keep several currencies;

- and confirm identity for private service access. In Ukraine, Privat24, a banking app and digital wallet, can confirm a user’s identity for Diia, the country’s digital ID and public service app.

The upside is huge. Yet wider use also brings more security risk. More users can make a wallet more attractive to criminals, and fraud losses can grow fast. That is why banks creating digital wallets and fintech firms face the same hard question: how to create a digital wallet that feels simple for users but stays very hard to attack?

>>> Let's break down the key considerations and step-by-step development process to help your business make decisions in crypto wallet development.

How To Create A Digital Wallet App Step By Step

This process shows how to create a digital wallet app, from early idea to real launch, without turning the build into a guessing game.

Step 1: Choose The Wallet Type

The wallet model affects rules, features, payment flow, and market reach. Pick it based on your users and business plan.

- Universal Wallet: Works across many providers and payment use cases. Think of PayPal or Google Pay. It often needs more legal approval, but gives the widest use range.

- Brand-Only Wallet: Runs inside your own product or service. Amazon Pay is a good case. It is usually easier to release, but it serves a smaller market.

- Partner-Based Wallet: Works with approved merchants and service partners. Paytm used this path before moving into a wider model. It gives a safe way to test demand.

- Digital Asset Wallet: Supports currencies like Bitcoin or Ethereum. It comes with different rules, but demand is growing among users who want crypto access. Some founders also research how to create a stablecoin for a more stable payment coin.

Start with one wallet type. Later, you can add more use cases once the first version proves real demand.

Step 2: Set The Wallet’s Core Functions

Too many features can drain time and money. Aim to solve one clear user problem very well.

Basic wallet tools usually include:

- User sign-up and profile control

- Send and receive money tools

- Payment records and receipts

- Basic safety settings

Add these larger features only after the MVP works:

- NFC tap payments for stores

- Bill and utility payment links

- Cashback and loyalty tools

- Multi-currency tools for overseas users

- AI automation spending notes and budget tips

A create digital wallet plan should be led by user research, not by every tool your team can build.

Step 3: Pick The Platform And Tech Stack

You need one major answer early: which stack will support a safe and stable wallet build?

Common choices include Flutter or React Native for cross-platform apps, NodeJS or Django for the backend, and links with Stripe, Firebase, and secure login standards like OAuth 2.0.

A strong backend also needs these parts:

- Cloud setup, such as AWS, Google Cloud, or Azure, for growth

- Databases that can protect payment records

- API design that lets you add new tools later

- Microservices to make fixes and updates easier

A clear create digital wallet development plan should use trusted finance APIs where they fit. A custom build is useful, but you do not need to rebuild every basic payment layer.

Step 4: Design The User Experience

People leave apps that look risky or hard to use. The interface must build trust and keep actions simple.

Strong design should focus on:

- Clear order and layout for payment steps

- Fewer taps for common actions like sending money

- Visible trust signs across the whole app

- Access support for users with disabilities

Study wallets like Venmo, Cash App, or strong local payment apps in your target market. Look at onboarding, payment confirmation, failed payments, and error screens.

Test clickable mockups with real users before coding starts. Good prototypes can save months of fixes later.

Step 5: Build Registration, Login, And Onboarding

The first few minutes decide whether users finish setup or quit the app.

Keep onboarding simple:

- Social login can cut friction

- Ask for details in stages

- Explain why each permission is needed

- Show value right after basic setup

Add strong identity checks without making new users feel blocked. Start with basic checks, then add deeper checks as user activity grows.

KYC rules change by country. Plan different check levels based on payment size and user location.

Step 6: Connect Payment Gateways

Gateway Connection links the wallet to the wider online payment gateway integration system. This step affects supported payment methods and transaction speed.

Popular gateway choices include:

- Stripe for global coverage and clear developer tools

- Razorpay for India-focused payment products

- Square for retail and face-to-face payments

- PayPal for broad trust and worldwide reach

A team planning how to create a digital wallet should look at more than one gateway. This helps reduce risk if one provider fails or does not fit a certain region.

Your payment design should handle gateway errors smoothly and give users another safe payment path when needed.

Step 7: Add Security Controls

A breach can break user trust and damage the whole business. Strong protection needs to be part of the build from day one.

Core safety controls include:

- End-to-end encryption for private data

- Two-factor login for account access

- Biometric checks on supported devices

- PCI DSS rules for card payments

- Routine audits and penetration testing

Fraud checks should use machine learning solutions development to watch payment patterns and flag risky activity.

Security is central to how to create a digital wallet that users can trust. A cybersecurity team can also help find hidden gaps before launch.

Step 8: Build And Test The MVP

A wallet MVP should prove the main value first. Do not try to ship every feature at once.

Your MVP should cover:

- User sign-up and basic profile setup

- Simple money sending and receiving

- Payment history view

- Basic security tools

- One main payment method link

Release the first build to a small user group. Learn from their behavior before adding bigger functions.

Track sign-up completion, transaction success, and user return rate after first use. These numbers show whether you are ready to create your own digital wallet at a larger scale.

Step 9: Test, Release, And Monitor

Finance apps need deeper testing than standard mobile apps. Money movement has to work every time.

Testing should include:

- Unit tests for separate parts

- Integration tests for payment paths

- Security tests for weak spots

- Load tests for high transaction volume

- User testing with real payment amounts

Release in stages. Start with beta users, then smaller regions, then a wider market release.

Watch payment success, app speed, and support tickets closely during the first launch phase.

When you know how to create a digital wallet, you also know the trade-off. The product must handle complex finance logic while still feeling simple for users. Solve one main problem well instead of packing the app with too many tools.

Top 12 Key Features For Digital Wallet App Development

The cost of a payment wallet depends on many items, and features play a big role. Businesses studying how to create a digital wallet should review these e-wallet tools one by one.

Payment History And Alerts

A well-built eWallet app lets users view past payments and purchases in a clear history. When money moves in or out of an account, the app should send instant alerts.

Many companies now build e-wallet products with several alert types for account activity. These may include email, push messages, and SMS.

A strong user-friendly feature is custom alert control. Users can choose what payment notices they want and how they want to receive them.

Bank Transfers

Most payment apps let users move money between bank accounts and mobile wallets. Businesses that send funds to clients, vendors, or partners, including overseas parties, often need multi-currency support.

Developers use secure APIs to create a safe payment flow. Banks and gateways often provide these links, so users can add money to the wallet or send it back to a bank account.

Bill Payments

Many users pay electricity, water, gas, property tax, and subscription bills through eWallets. A digital payment system can let them pay right away or set future payments through approved service partners.

These partner links can shape the total wallet build cost. Pricing may rise when you add smart billing tools or live payment matching.

Virtual Card Management

Modern wallets let users link and control debit or credit cards without carrying plastic cards. Many use tokenized virtual cards stored under safety rules like PCI DSS, the Payment Card Industry Data Security Standard.

Developers add strong encryption and login checks to keep card data safe. More complete wallet apps let users see card transactions, set limits, and add or remove cards in a few taps. Simple card linking and removal can affect the total smart contract wallet app cost.

Contactless Payments

Many retail chains in the U.S. now accept NFC and QR code payments from shoppers. If your business wants contactless transactions, a digital wallet can add these modern payment methods.

Businesses that want fast, safe, and easy payments should plan this part during eWallet app development. The final cost of QR code tools depends on several build choices.

A basic scan screen costs less than dynamic QR code creation. The app platform, such as iOS, Android, or both, and the vendor’s location can also affect the final price.

Secure Login And User Checks

Security matters most when you build a FinTech app. Your mobile payment product needs proper user checks to keep transactions safe.

Face login, PINs, two-factor codes, and fingerprint checks help confirm that only real registered users can access the payment system. A skilled developer can add modern biometric login during digital wallet app development.

Self-Registration

A simple self-registration flow can help more users start using your wallet. Build an app that lets people join quickly with little friction, so adoption and engagement can grow.

For smooth registration, the app should work on both Android and iOS. After install, users often complete KYC by uploading digital ID files. The flow may include OTP checks, login setup, and bank or card linking.

A safe and easy self-registration flow can raise the cost and complexity of the eWallet platform.

Rewards And Deals

Loyalty points, cashback, and payment discounts can keep users active inside mobile wallet apps. These tools can support repeat use and give your app a clearer place in a crowded market.

Business owners who build an e-wallet often work with skilled IT partners to plan these functions well. Clear product goals help them decide which rewards belong in the app. You can also market the wallet through cashback, referral codes, or loyalty campaigns based on your model and users.

User Spending Dashboard

A full eWallet app can show many details through a useful dashboard. This may include upcoming bills, planned payments, and user spending patterns.

During digital wallet app development, teams can add a dashboard that helps users track expenses and manage money better.

Chatbot Support

Users of payment apps often have questions during or after a transaction. A chatbot inside the FinTech platform can answer basic questions and guide users through app actions.

Adding AI agent frameworks to a payment app can raise development cost. The price may increase further if you add tools like voice search.

Multi-Currency Support

Some eWallets are built for users in different countries. If you want to serve global customers and help them pay across markets, the wallet should support several currencies.

Multi-currency support can make your digital wallet more useful for international users. It may also help your business stand apart from payment apps that only serve local users or the U.S. market.

P2P Payments

Virtual wallets work well when users send money to people in their contact list. A P2P feature lets users send and receive money directly. Splitting bills or paying a partner in a shared business task becomes fast and simple.

This feature needs a stable and high-performing e-wallet. A clear digital wallet development process helps these payments work well. It is wise to work with an IT vendor that understands how to turn old payment flows into modern wallet apps.

Key Benefits Of Building A Digital Wallet App For Business

Digital wallets are gaining strong use, and the e-wallet market is set to keep growing. If you are learning how to create a digital wallet for your business, these benefits show why the investment can make sense.

Create New Revenue Channels

Your own wallet gives you room to test different income models. You can earn from transaction fees, partner deals, or paid add-on services. You can also sell the e-wallet as a white-label product, so other companies use your technology under their own brand.

Own Customer Data And Payment Behavior

An e-wallet gives your business direct access to customer payment data. This control helps you understand buying habits, user needs, and spending patterns, then make better business choices.

Build A Branded Payment Experience

A custom e-wallet lets you shape a payment flow that fits your brand. The interface, screens, and user journey can match your identity, helping users remember your business and return more often.

Reach Customers Across Borders

Digital wallets can support cross-border payments and currency exchange. This helps businesses enter new markets and serve customers outside their home country.

Keep Customers Coming Back

Retailers and service firms can build closed wallets that work only inside their business. These wallets support private rewards, discounts, and deals that give customers a reason to keep using the brand.

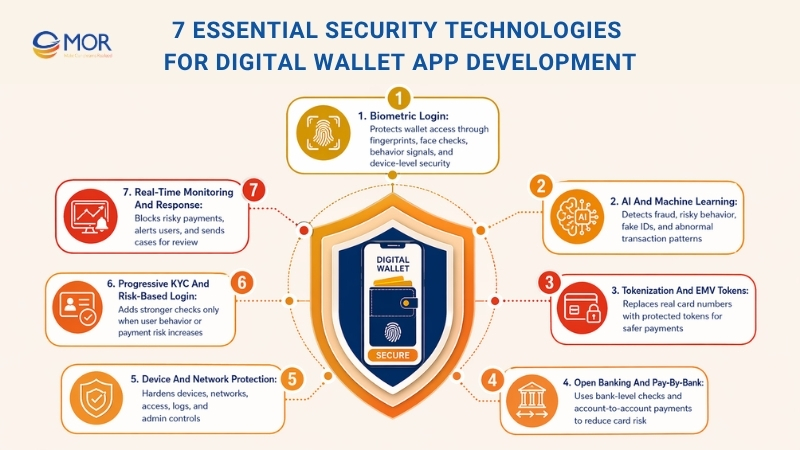

7 Essential Security Technologies For Digital Wallet App Development In 2026

Many startups and fintech teams are exploring how to create a digital wallet with fast payments and stronger user protection. Payment app innovation is pushing wallet products to become safer, quicker, and easier to use. These security tools help real users move smoothly while making attacks harder.

Biometric Login

Biometric login, such as fingerprint scans, face checks, and biometric KYC, is now a main safety layer in crypto exchange development. According to ResearchAndMarkets, biometrics is one of the fastest-growing mobile wallet features because users need quick access and live protection against account takeover.

Major wallets like Apple Pay, Google Wallet, and Alipay use biometrics because they protect accounts with very little user friction.

Biometrics now go beyond unlocking a device. Behavioral biometrics, including typing style, touch force, and motion, can spot risky behavior in the background. This lowers fraud without slowing users down. In markets with heavy QR use and high transaction volume, biometrics add a key check before payment. As wallets move into banking, loyalty, and currency tools, biometrics are now a core part of a safe user flow.

Interesting fact: according to Statista, biometric systems measure unique body traits and have supported identity checks for more than 200 years.

Pro tip: Keep biometric checks on the user’s device, not in the cloud. Pair them with a device PIN and live risk scoring. Ask for extra login checks only when activity looks unusual or risky. This keeps normal payments quick while adding layered fraud defense.

AI And Machine Learning

AI is now widely used in financial services around the world. In the UK, 75% of financial services firms already use AI, and another 10% plan to adopt it within three years. Common uses include fraud checks, AML, cybersecurity, and live analytics, all of which matter for mobile wallet work.

Modern AI tools can catch fraud and support lending choices. One use is AI in credit scoring, where the system reviews user risk and can improve approval decisions.

Starling Bank’s AI scam-detection tools and generative AI integration detection pilots show how banks can place AI inside real customer payment flows.

AI systems study user behavior, device data, transaction speed, and past fraud signs to catch unusual actions right away. Modern information sets used in machine learning can spot account takeover, fake IDs, and bot attacks. They can also cut false declines, so real users are not blocked too often.

Pro tip: Use AI to watch payments and user behavior in real time during e-wallet app development, but do not depend on AI alone. Pair risk scores with biometrics, device checks, and extra login steps only when activity looks suspicious. This keeps normal users moving while stopping fraud attempts.

Tokenization And EMV Tokens

Tokenization protects payments by replacing the real primary account number, or PAN, with an EMV payment token. If someone intercepts that token, it has no useful value on its own. Unlike static card data, tokens work with changing transaction cryptograms, so every payment is unique. If a token or payment payload is stolen, it cannot be reused. Domain controls can also limit a token to one device, merchant, or channel, which cuts fraud risk.

In mobile wallets, wearables, IoT devices, and saved-card systems, tokenization separates the payment account from the card or device. It can also be added across platforms through web app development services for a steady safety and user flow. One PAN can connect to many tokens across devices, so losing a phone does not mean issuing a new card. Reissued cards also do not always need every device to be set up again. Short-use keys and step-up checks during setup make unauthorized token activation harder.

Tokenization improves safety, but it can create some operation issues. EMV tokens often do not match the last four digits of the real card, so users may feel confused when checking receipts or statements. Merchants may also need to adjust loyalty, analytics, and fraud systems that once used the PAN to identify users. The Payment Account Reference, or PAR, helps link tokens to one account without exposing private card data.

Open Banking And Pay-By-Bank

Open banking and account-to-account rails are becoming a safer card alternative. Pay-by-bank uses bank-level login checks and reduces dependence on card networks, which can lower chargebacks, raise payment success, and make onboarding more trusted.

A Token.io and Open Banking Expo survey found that 59% of banks and 90% of payment service providers either provide or plan to provide pay-by-bank services. Merchant interest is also strong, with 91% saying they are interested in A2A payments. Providers like Adyen, Stripe, Tink, Plaid, and TrueLayer support A2A rails that lower card fraud exposure.

Pro tip: When building a digital wallet, add open banking rails for checked payment flows. Use bank-sourced identity signals to support stronger KYC, and keep card payment fallback so all users can still pay.

Device And Network Protection

According to CISA, many attacks take advantage of weak device and network settings. For secure wallet apps, visibility and hardening matter. Teams can catch early signs of risk through traffic checks, setting changes, and user activity logs. Central encrypted logging, plus clear separation between user networks, admin areas, and public services, makes it harder for attackers to move inside the system and reach payment data. Out-of-band control for key devices also keeps admin access away from live traffic.

Hardening also means using modern protocols, multi-factor login, role-based access, and fast patches for firmware and software. Turning off unused services and giving users only the access they need can reduce attack paths. These practices help businesses trust the user, device, and channel before allowing payment, which lowers fraud and account takeover risk.

Progressive KYC And Risk-Based Login

Progressive onboarding lets users start with low-risk actions first, then complete stronger identity checks as their usage or payment value grows. Risk-based login works with this flow, so the system asks for stronger checks only when behavior looks unusual. According to Juniper Research, AI identity checks may cut average onboarding time from over 11 minutes in 2023 to under 8 minutes by 2028. This helps fintech firms keep sign-up smooth while protecting against fraud and fake identities.

Pro tip: When building a digital wallet, use account tiers such as guest, verified, and verified plus. Automate ID and document checks where possible, and send only edge cases or risky transactions to manual review. Add ongoing AI risk scoring so safer users move smoothly while risky activity gets stopped.

Real-Time Monitoring And Response

Detection alone is not enough. Build automated response flows so the wallet can block a payment, freeze a payout, request extra login, send a risky case to a human team, and alert users in real time. Modern fraud tools can connect with fraud APIs, case tools, and chargeback systems.

Pro tip: Use an event bus for risk signals, set clear review time targets, and give real users a simple recovery or appeal path.

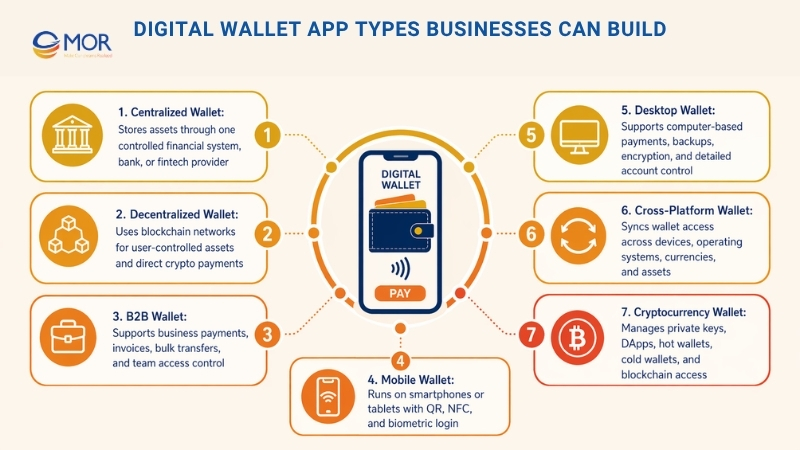

Digital Wallet App Types Businesses Can Build

Fast fintech growth has pushed businesses to support safer money transfers and stronger payment tools. That is why different wallet models now exist for different business needs.

Wallet app types can vary by storage model, use case, and device platform. This choice affects app functions, security, and the way the product is built.

If you are learning how to create a digital wallet, start by comparing these common types:

Centralized Wallet

Storage type is one way to separate centralized and decentralized wallets. In a centralized wallet, one financial company, such as a bank or fintech firm, controls the wallet system.

It can hold financial assets on central servers and usually includes these traits:

- Keeps funds in protected storage

- Lets users send money through mobile payments

- Shows users their payment history

- Connects with banks and finance systems

Common examples include PayPal and Apple Pay.

Decentralized Wallet

The main difference is that a decentralized wallet runs on a blockchain network rather than one central system.

This wallet type often includes:

- User-controlled asset storage

- Direct P2P payments

- DeFi access

- Cryptocurrency support

- A higher level of privacy

B2B Wallet

A B2B wallet is built for business use. This type of wallet app supports business payments, including bulk transfers, invoices, and payment tracking for small and mid-sized firms.

Features include:

- Bulk payment handling

- Invoice and payment tracking

- Accounting software links

- Team access control

- Safe business-to-business transfers

A common example is Payoneer.

Mobile Wallet

Mobile, desktop, and cross-platform wallets are grouped by device support. A mobile wallet is built for smartphones or tablets.

This type usually includes:

- Mobile-friendly screens

- QR code scan tools

- NFC support

- Mobile banking links

- Biometric login

Desktop Wallet

Desktop wallets run on computers. They usually connect standard desktop screens with gateways and online payment systems.

Common traits include:

- A larger interface for detailed control

- Links with software or mobile devices

- Two-factor login and point-to-point encryption

- Wallet data backup and recovery

- Support for fiat money and crypto assets

Cross-Platform Wallet

A cross-platform wallet works across different devices and operating systems.

It often includes:

- Device-to-device sync

- Backup and restore across platforms

- Support for many currencies and assets

Cryptocurrency Wallet

A cryptocurrency wallet supports blockchain-based financial transactions and needs strong safety controls for digital assets.

Common traits include:

- Private key storage

- DApp access

- Hot and cold wallet options

This is also where users often ask how to create a digital wallet for cryptocurrency, since the app must manage private keys, blockchain networks, and asset access with care.

Choosing the right mobile wallet type matters for the business. It shapes security, user experience, and growth options for financial services.

Blockchain, biometric login, and system integration also affect whether your business keeps pace with market needs and follows legal rules.

Next, we look at the business gains of wallet app development, from lower operating cost to wider market reach, and why it can be a strong fintech move.

Security Compliances For Digital Wallet App Development

To build a legal digital wallet app, follow the security rules and data laws in your target region. In the United States, e-wallet providers must follow a mix of state and federal rules for collecting, storing, and processing financial data.

If you are learning how to create a digital wallet for regulated use, these compliance areas matter during eWallet app development:

Data Privacy Laws

Your app must follow accepted privacy laws, such as the California Consumer Privacy Act, or CCPA, in the U.S. These rules require clear handling of how user data is collected, used, and shared.

Multi-Factor Login

Add multi-factor login to create another security layer. This can include face scans, fingerprints, one-time codes, and PINs. Users expect these checks, especially on iOS devices, because they confirm identity beyond a password.

Safe Data Transfer

Data needs protection while moving and while stored. All communication between the app and backend servers should use strong encryption. Protocols like SSL, TLS, or VPNs can help stop leaks during transfer. This keeps private data like login details and payment records safer.

Safe Data Storage

Use hashing and encryption to protect financial data stored inside the app or backend. If a breach happens, protected data should stay unreadable without the right keys.

Fraud Protection

The app should detect risky behavior and possible fraud. Real-time payment monitoring, IP checks, and alerts can help stop fraud and block unauthorized access.

PCI DSS Rules

If your wallet handles card payments, confirm that it follows the Payment Card Industry Data Security Standard, or PCI DSS. These rules help protect cardholder data during payment processing.

Security Audits And Updates

Cyber threats change often. The app needs routine audits, fast patches, and system updates to stay protected. Careful security work during and after eWallet app development can help prevent breaches.

Technology Stack For Ewallet App Development

Want to build a safe, mobile-friendly, and easy payment product? Teams researching how to create digital wallet products often start with these common eWallet technologies.

Category | Tech Stack |

Phone Verification | Nexmo |

Frontend | Angular, CSS, JavaScript, and HTML5 |

Database | HBase, Cassandra, and MongoDB |

Cloud Environment | Salesforce, Google Cloud, AWS, and Azure |

Push Notifications | Push.IO, Amazon SNS, Twilio, Urban Airship |

Real-Time Analytics | Hadoop, Apache, and Spark |

QR Codes | ZBar Code Reader |

Digital Wallet Development Cost In The US Market

The estimated cost of e-wallet app development can change based on the features you add to the payment platform. Businesses learning how to create a digital wallet should treat these numbers as planning ranges, not fixed prices.

Feature | Focus | Estimated Cost (USD) |

Payment History And Alerts | Show past payments, send push, email, or SMS alerts, and allow custom alert settings. | $8,000-$12,000 |

Bank Transfers | Add safe API links for bank-to-wallet transfers, with multi-currency support when needed. | $15,000-$20,000 |

Bill Payments | Let users pay or schedule utility and service bills through third-party aggregator links. | $8,000-$12,000 |

Virtual Card Management | Support tokenized cards, card linking and removal, plus transaction views. | $10,000-$15,000 |

Contactless Payments | Add QR code and NFC payment support based on platform and device needs. | $4,000-$8,000 |

Secure Login And User Checks | Add two-factor login, face checks, biometric login, and PIN protection. | $8,000-$15,000 |

Self-Registration | Build onboarding with OTP, document upload, and KYC checks for Android and iOS. | $5,000-$8,000 |

Rewards And Deals | Add loyalty points, cashback, referral codes, and custom business rewards. | $10,000-$15,000 |

User Spending Dashboard | Add expense tracking, budget views, and visual money reports for users. | $8,000-$12,000 |

Chatbot Support | Add an AI support bot for basic questions, with voice search as an optional add-on. | $5,000-$8,000 |

Multi-Currency Support | Add currency exchange, global wallet support, and FX rate links. | $12,000-$18,000 |

P2P Payments | Let users send instant money to contacts, split bills, and add optional secure messages. | $10,000-$15,000 |

Most Popular Examples Businesses Can Learn From

Many e-commerce companies now use contactless payment to manage transactions faster. If your enterprise or startup needs a wallet system, build one that fits your business model. These popular apps can teach useful product lessons for teams learning how to create a digital wallet.

Apple Pay

Launched in 2014, Apple Pay is an NFC-based mobile wallet for iPhone, Apple Watch, iPad, and Mac. It stores payment cards through tokenization, uses Face ID or Touch ID, and supports in-store, in-app, and online payments while protecting privacy.

Apple Pay is estimated to have 659 million users worldwide and about 63.9 million users in the U.S. alone. Building a wallet like Apple’s payment system may cost $40,000-$150,000+, or more, depending on the build.

Google Pay

This payment app has moved into the Google Wallet platform. It supports NFC tap-to-pay, QR payments, P2P transfers, bill payments, loyalty tools, encryption, tokenization, and biometric or PIN checks on Android and iOS.

Launched in 2015, Google Pay has about 250 million users worldwide. Reports also estimate that 57 million Americans may use the platform by 2028.

Apps similar to Google Wallet may cost $100,000-$300,000 to build, based on scope and complexity.

PayPal

PayPal is a global digital wallet and online payment service with about 436 million users. It supports safe P2P transfers, in-app payments, online purchases, QR code and POS payments, multi-currency use, crypto options, buyer protection, and One Touch checkout.

Many e-commerce firms choose this type of app model for fast and trusted payments. A similar digital wallet app may need a budget of $150,000-$300,000 on average.

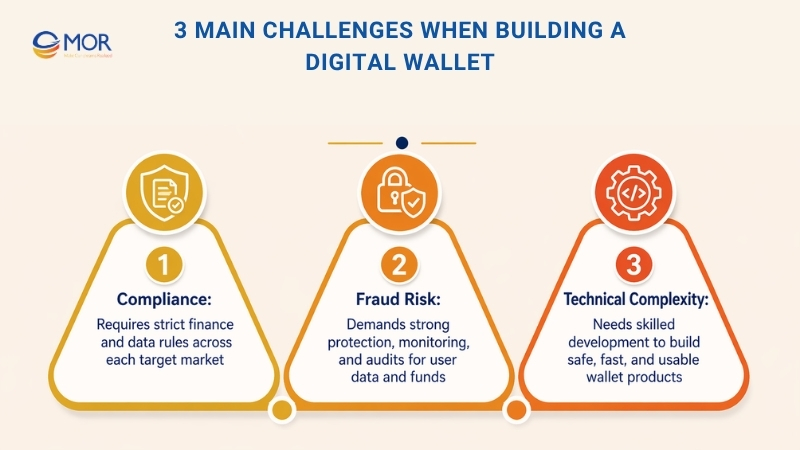

3 Main Challenges When Building A Digital Wallet

Launching a wallet can be a strong business idea, but it comes with real risks. Businesses researching how to create a digital wallet should plan for these issues early.

Compliance

A wallet is harder to set up than many other apps because finance and data rules are strict. These rules also change by country and region. Knowing how to set up the app is not enough. You need to understand the legal rules in each target market and build the product around them.

Fraud Risk

Payment fraud existed long before online finance, and digital systems did not remove the problem. You need strong security controls to protect user data and funds. Regular audits also help find weak spots before attackers do.

Technical Complexity

A wallet app needs skilled developers and a strong grasp of current payment technology. Work with a team that can build digital wallet products that are safe, fast, and easy to use.

Build Your Digital Wallet With MOR Software

If you are deciding how to create a digital wallet, MOR Software can help turn the plan into a working product. We build mobile apps, web platforms, backend systems, cloud architecture, payment integrations, QA flows, and long-term support models for businesses that need reliable software.

Our team can support the full digital cryptocurrency wallet development process, from business analysis and UI/UX design to development, testing, integration, and maintenance. For companies asking how to create a digital currency wallet or how to create a digital wallet for business payments, this full-cycle support of crypto wallet development company helps reduce gaps between strategy, design, security, and launch.

MOR Software also works with finance, banking, retail, healthcare, manufacturing, and enterprise teams. That mix matters when a wallet must connect with real business systems, not just payment screens. We can help you create digital currency wallet products, mobile wallet apps, and custom fintech platforms that fit your users, rules, and growth plan.

Conclusion

Building a digital wallet takes more than clean screens and fast payments. You need the right wallet type, secure architecture, clear KYC flow, trusted payment gateways, fraud checks, and a product plan that fits your business model. Once you understand how to create a digital wallet, the process becomes easier to manage and safer to scale. Contact MOR Software to discuss your secure digital wallet project today.

MOR SOFTWARE

Frequently Asked Questions (FAQs)

How long does it take to develop a wallet app?

The timeline depends on the app’s scope, platform support, feature list, and security needs. A simple wallet may take a few months, while a larger product with deep integrations can take six months or more. Teams that already have a clear plan for how to create a digital wallet can usually move faster because the product scope is easier to manage.

Can you provide an example of the innovative use of a digital wallet?

A strong use case is public transport payment. Many cities let riders pay by tapping a phone at gates, buses, or train stations. This makes travel faster because users no longer need paper tickets or stored-value cards.

How much does it cost to create a digital wallet?

The cost depends on features, app platforms, backend needs, compliance work, and security controls. A basic e-wallet can begin near $20,000, but a larger platform with payment gateways, KYC, fraud checks, and analytics can cost several hundred thousand dollars.

What technology is used for mobile wallets?

Mobile wallets often use NFC for tap payments and QR codes for scan-based payments. They also use APIs, cloud services, encryption, tokenization, biometric login, and secure databases to process payments and protect user data.

What technology should we pick for implementing mobile payments?

The right choice depends on your users, payment setting, security needs, and local infrastructure. NFC works well for tap-to-pay at stores, while QR codes can be cheaper and easier to roll out in many markets. Your choice should match how your customers already prefer to pay.

How to make money with digital wallets?

Digital wallets can earn money through transaction fees, premium subscriptions, partner offers, merchant services, white-label licensing, and value-added tools. The best model depends on your users, wallet type, and how often people use the platform.

Share

Rate this article

0

over 5.0 based on 0 reviews

Your rating on this news:

Name

*Email

*Write your comment

*Send your comment

1